FHA Construction Loan Down Payment: What You Need to Know

Posted on: September 12, 2024

Summary

FHA construction loans are ideal for homebuyers and builders seeking to construct new homes with a low-down payment, typically around 3.5%. These government-backed loans are divided into two phases: the construction phase and the permanent mortgage phase. The down payment plays a crucial role in determining the overall loan value, and a higher down payment can lower the loan-to-value ratio, reduce interest rates, and increase borrower equity. Key factors influencing down payments include credit scores, loan amounts, property value, debt-to-income ratios, and builder approval by FHA. Borrowers should be aware of potential challenges such as construction delays, approval hurdles, and coordination between the construction and mortgage phases. Understanding these aspects can lead to better loan terms and successful real estate investments. Consult Munshi Capital for tailored financial advice and support.

FHA construction loans are ideal for homebuyers and builders who want to construct new homes; they are government-backed and are divided into the construction phase and the permanent mortgage phase. The FHA construction loan down payment is considered the key aspect to determine the impact on overall loan value. In recent years, the trend for the down payment percentage has been around 3.5%. The down payments are helpful for both borrowers and lenders; for lenders, it helps mitigate the risk, and for borrowers, it reflects the financial stability required for loan approval. There is no maximum down payment limit set, but borrowers who go for a higher down payment should consider the associated impact. A higher amount of down payment can reduce the loan-to-value ratio and help in getting better interest rates and loan terms; it also increases borrowers’ equity with reduced cost of FHA mortgage insurance premiums.Let’s understand all the associated terms and factors of FHA construction loan down payments in this blog.

Understanding Credit Score and Down Payment Requirements

Credit score and down payment are crucial requirements to secure an FHA construction loan, below are key pointers:

To avail of an FHA construction loan, borrowers need a minimum of 580 credit score to get 3.5% of the down payment. There may be lenders that can increase the down payment percentage if the credit score is between 500-570 to qualify for the loan.

Having a high credit score results in a better interest rate, flexible terms, and a lower down payment percentage, which can reduce the overall loan costs.

Borrowers need to improve their credit scores by paying bills on time, reducing the balance of their credit card, regularly monitoring credit card reports, avoiding any new inquiries to create new credit accounts, etc., to get better down payment terms.

Impact of Down Payment Percentage on FHA Construction Loan

Let’s understand these two different scenarios and their impact based on the down payment percentage on the monthly payment and total interest paid:

Scenario

Home Purchase Price

FHA Loan Down Payment (%)

Down Payment Amount

Loan Amount

Monthly Payment Impact

Total Interest Paid Impact

#1 Minimum Down Payment

$500,000

3.50%

$17,500

$482,500

Higher

Higher interest

#2 Higher Down Payment

$500,000

10%

$50,000

$450,000

Lower

Lower interest

Note: The term period has been taken as 30 years, and interest depends on the principal amount, if the principal amount is higher, interest is higher, and vice-versa.Discover how FHA construction down payments work, key factors affecting them, challenges, and solutions to support your successful real estate investment journey.

“FHA Construction Loan vs Conventional Construction Loan”

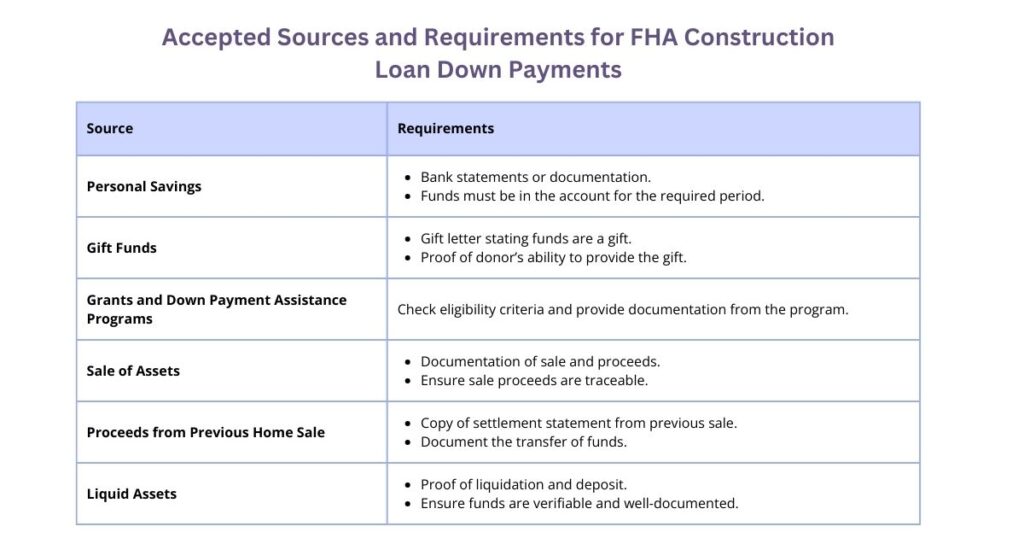

Source of Down Payments Accepted Under FHA Construction Loans

The table below gives an insight into different sources the borrower can use to make the down payment for the FHA construction loan:

What Factors Influence FHA Construction Loan Down Payments?

Various factors can influence FHA construction loan down payments from loan amount to type of construction, as discussed below:

Loan Amount and Property Value: The down payment changes as the loan amount increases, and if your value of property is lower than the loan amount, then the down payment increases.

Debt to Income Ratio: FHA recommends a DTI ratio of 43% or lower; if it is more than the limit, then the lender can ask for higher down payments.

Project Scope and Requirements by Builder: Down payment is affected if the builder is not approved by FHA or there are errors in the construction plan. Also, project complexity affects down payments.

Property Location and Type: If you are looking for an FHA construction loan for investment properties that may not meet FHA requirements, then higher down payments may be implied, the same with high-cost and low-cost areas.

FHA Loan Limits:If your construction loan amount exceeds the limit set by the authority as per the area, then excess down payments need to be paid. The base limit calculation for high-cost areas can be done as: High-Cost Limit = Median Home Price * % of the median home price.

FHA Construction Loan Challenges Borrowers Need to Address

Listed below are a few challenges with FHA construction loans that borrowers should look for:

To be eligible for FHA construction loans, the chosen builder should be FHA-approved; otherwise, it can limit your options. The builder should meet set standards for qualification of construction and completion within the timeline.

Construction-related projects can induce overrun costs due to delays that can impact financial stability; it is advised to keep a minimum of 15% as a contingency budget for handling the delays.

To get an FHA construction loan, HUD’s minimum property standards should be met. To avoid the delay, it is better to have a pre-inspection so the pitfalls can be worked upon and a better down payment percentage.

FHA construction loans are divided into “construction loans” and “permanent mortgage loans,” so coordinating with the two can be challenging. Find a lender that can help in a seamless transition from construction to a permanent mortgage loan with a one-time close loan.

Conclusion

FHA construction loans are a viable option for homebuyers or builders looking for a low-down payment option, as they help people who have less savings but good financial stability to pay monthly mortgages. Before going for the FHA construction loan, it is important to consider what factors can impact the down payment percentage, like project scope, lender policies, additional costs such as closing costs, loan limits based on the region, approval of the builder by FHA, and more, to make an informed decision.To get better-tailored advice and financial solutions like loan comparison tools, down payment assistance, personalized support, etc., for your FHA construction loan, consult Munshi capital and get better financial results.Read More: FHA Loans for a Second Home: Requirements and How to Qualify

Frequently asked questions

1. Do I need to give mortgage insurance for the FHA construction loan down payment?MIP, or Mortgage insurance premium, is required for FHA construction loan down payment; around 1.75% of the loan amount is the upfront MIP, with an annual MIP requirement also. 2. If I am living in a high-cost area, are there any special considerations for an FHA construction loan down payment?The 3.5% down payment requirement does not change in high-cost areas due to increased FHA loan limitations. It’s critical to understand the local FHA loan limits since you could have to obtain additional financing or make a larger down payment if your loan amount exceeds these limits.3. Is using funds from a 401(k) or IRA withdrawal acceptable for an FHA construction loan down payment?Yes, you can use funds from a 401(k) or IRA withdrawal for an FHA construction loan down payment, subject to taxes and penalties if withdrawn earlier.4. What is the maximum down payment allowed for an FHA construction loan?As such, there is no set maximum down payment limit for an FHA construction loan; if borrowers want, they can pay more than 3.5%, which will reduce down payments, loan amount, etc.5. What is the eligibility requirement for a down payment assistance program?The borrower should not have owned a home in the last 3 years, have a minimum credit score of 620, completion of homebuyer education course, and earn below a specific percentage set of the Area Median Income (AMI).6. What is the mortgage insurance upfront percentage for an FHA loan California?FHA loans in California estimated mortgage insurance upfront percentage is around 1.75% of total loan amount.

About the Author

Amish Munshi

I'm Amish Munshi, a mortgage lender with over 20 years of experience in the world of real estate lending. I love breaking down complex loans—like hard money loans, DSCR loans, FHA loans, and other private financing options for real estate—into simple terms so you feel confident at every step of your journey. Whether you're buying your first home or expanding your investment portfolio, I'm here to guide you with the right insights and expertise to help you reach your financial goals.