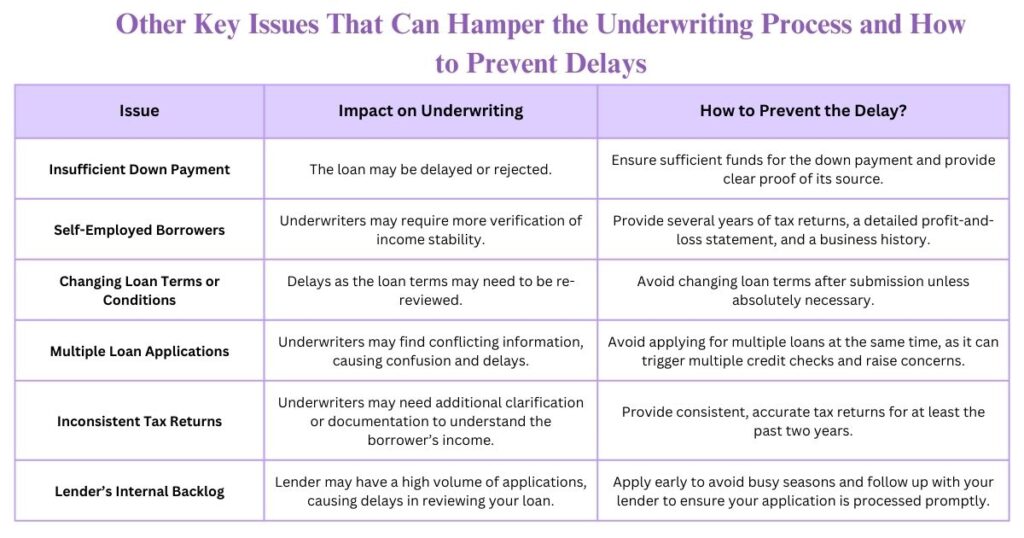

Table of Contents

ToggleIntroduction

Some applicants view the underwriting procedure as the last obstacle to obtaining a loan, and for some, it feels like an endless wait. Underwriting delays can result in lost opportunities as well as financial hardship for both lenders and borrowers. If you are a first-time homebuyer or a seasoned investor, this blog will help you understand key factors that cause delays in the underwriting process and actionable solutions to make your financial journey more efficient.

Uncover the Top 5 Reasons Behind Underwriting Delays and Expert Tips to Prevent Them

#1. Incomplete Documentation or Inaccurate Information

In order to make an informed decision, underwriters need complete and accurate information in your documents; any discrepancy from recent pay stubs missing to unverified large deposits in bank accounts to the absence of homeowners association documents for a property can cause the need for additional verification and delay in the process.

How to Prevent the Delay?

- For a more seamless process, you can create a checklist of all documents required, from pay stubs to bank statements to tax returns. It is always beneficial to provide additional documents for verification of recent large deposits or transactions.

- If you are starting a new job, then keep documents like a contract, recent pay stub, offer letter, and more ready with you.

- Make sure your tax returns are completed, including all schedules and forms, as lenders frequently need the last two years’ data. Address and provide an explanation for any anomalies in your tax filings to avoid future delays.

- Double-check all small details like personal address, contact number, email ID, etc., as discrepancies in these details can delay your underwriting process.

#2. Regulatory and Compliance Challenges

Imagine you have applied for a loan with an attractive interest rate. Everything seems to be going well until the underwriter notices a regulatory roadblock due to a new compliance requirement that the lender must adhere to or a recent modification in lending regulations.

Now, underwriters need to analyze these new rules, request more supporting documents, or reevaluate the application. These delays are unavoidable if people are unaware of these changes or if documents do not align with the recent regulatory requirements.

How to Prevent the Delay?

- Be ready for AML (anti-money laundering) inspections (if needed)

- Verify your eligibility for loans supported by the government.

- Stay up to date with industry news and local state regulations.

- Be open and honest about your work position.

- Observe the rules unique to your property.

- Check the lender’s preparedness for compliance.

- Be ready for changing financing requirements.

- Keep your financial profile steady.

- Answer regulatory questions as soon as possible.

#3. Discrepancy in Credit Report

You feel confident with your credit financial history, but when it is submitted for underwriting, there are discrepancies that underwriters highlight, like a missed payment that you thought was settled. Red flags like these can lead to a delay in the process due to additional verification or clarifications from the credit bureau or you.

How to Prevent the Delay?

- It is important to get a credit report in advance to check if there are any discrepancies so they can be addressed in a timely manner. If there are any errors in the credit report, they can also be resolved by consulting the credit bureau.

- If you see any unusual activity in your credit report, like late payments, then you can write a clear explanation and submit it with your loan application.

#4. Property Appraisal Issues

Property appraisals help evaluate if the value of the property aligns with the loan amount. If your appraisal is lower than the expected value, then the underwriter may require documents for additional checks or go for changing loan terms, which can cause delays in the underwriting process.

How to Prevent the Delay?

- Select an experienced appraiser for fair property evaluations.

- To make sure the property is worth enough and to prevent unpleasant surprises later on, think about getting a pre-appraisal done before applying for a loan.

- Make sure the property is in good condition with necessary improvements and repairs so you don’t get a lower property value.

#5. Lack in Communication

Underwriting delays can be caused by poor communication between all important parties like the lender, title companies, underwriter, appraiser, etc. For example, you have sent all the required paperwork for your loan, but days pass, and you never hear back from the underwriter or lender.

Now, you are left wondering why the application is not moving forward. Here, the entire loan procedure may be delayed if loan officers/underwriters lack communication for your inquiries or other clarification.

How to Prevent the Delay?

- It is important to be responsive to your underwriter regarding any change in documentation, financial status, or any important information that can cause delay.

- With your lender, having a clear communication channel is important; the channels can be in the form of emails, secure online portals, messages, and more.

Pro Tips for Borrowers to Speed Up the Underwriting Process

- Provide digital documents for a much faster process, as some lenders have secure portals for quick and easy submissions.

- A lot of lenders use particular appraisers. It can save time by preventing scheduling delays or last-minute appraiser selection if you have the choice to request an appraiser in advance or use the lender’s preferred vendors.

- During the underwriting process, avoid doing unexplained or large transactions, as underwriters may ask you to give documents for the transaction made, causing a delay in the process.

- Make sure the title report is prepared and does not include issues such as outstanding liens or claims if you’re buying a house. When the title company confirms the property throughout the underwriting process, this proactive measure can prevent you from being delayed.

What Tips Can Lenders Use to Speed Up the Underwriting Process?

- Implement technology solutions like automated underwriting systems

- Compile a standardized list of required documents as per the loan type with clear guidelines

- Maintain a dedicated communication channel

- Pre-underwriting files can help in detecting issues before going to the formal underwriting process

Why Wait? Eliminate Roadblocks in Your Financial Journey Now

We understand that underwriting delays can be a major roadblock in your financial journey. Our expertise helps you in guiding through every step of the mortgage process, from ensuring that all documentation is complete with accurate information to seamless communication so no unnecessary holdups come in between. Connect with us today to streamline your loan application process.

Also Check: The Future of Real Estate: Emerging Trends in Property Investment

Frequently Asked Questions

- Can a high DTI ratio affect underwriting timelines?

Yes, because it raises questions about the borrower’s capacity to handle new debt, which can cause underwriting to be delayed. Underwriters could demand further actions, such as confirming income or asking for more supporting documents.

- What are the benefits of working with an experienced lender to avoid underwriting delays?

Working with experienced lenders helps handle the issues more promptly, as they have reliable networks and loan program knowledge and can resolve complex issues more efficiently, preventing the underwriting delay for borrowers.

- In which loans are underwriting delays more common?

Underwriting delays are commonly seen in loans like jumbo loans, non-conventional loans, construction loans, investment property loans, and self-employed borrower loans.