Hard Money Loan Rates in California: What Borrowers Should Know

Posted on: September 19, 2024

Summary

Hard money loans provide quick capital for California real estate investors, especially those with weak credit. Rates range from 9.5% to 14% in 2024, influenced by factors like location, lender risk, loan amount, and the exit strategy. Borrowers in high-demand areas like Los Angeles may face higher rates. Understanding fees and costs is crucial. Partnering with experts like Munshi Capital helps investors navigate negotiations and market dynamics to maximize returns.

The real estate market in California is one of the most dynamic and competitive in the United States. With rapid property appreciation and substantial growth, there is a rising demand for fast and flexible financing options like hard money loan, which provide quicker access to capital. Unlike conventional financing, which prioritizes creditworthiness and a strong financial portfolio, hard money loans are asset-based, using property as collateral.

These loans offer swift and adaptable financing but typically come with higher interest rates. As of 2024, high-demand cities like Los Angeles and the Bay Area are expected to see interest rates ranging from 9.5% to 14%, driven by intense competition and increased lender risk compared to traditional financing.

This blog explores how to navigate hard money loan rates in California high-value real estate market to maximize long-term financial benefits.

What are Hard Money Loan?

Hard money loans are asset-based, quick, and flexible financing products with a shorter timeline.

These loans are a boon for borrowers with a poor credit history or weak financial portfolio who do not qualify for traditional financing since hard money lending heavily focuses on the real estate involved.

In competition-driven real estate markets like California, hard money loans are high in demand to take advantage of quicker financing to seize lucrative opportunities.

Factors affecting hard money loan interest rates in California

Let us understand the various key factors that are crucial for borrowers to secure favorable terms and how these considerations majorly influenced the hard money loan interest rates:

#1 Location of the Property

Metropolitan areas like Los Angeles and the Bay Area attract higher rates of interest as they are high in demand and promise lucrative property appreciation and a competitive edge in the dynamic real estate market of California.

Hard money lenders in California consider these scenarios as an equal opportunity for higher risks and even higher returns.

#2 Lender’s Risk Appetite

Lenders with a higher risk-taking capacity will be willing to offer loans to newcomers, risky investors, or in projects involving distressed real estate by charging higher rates of interest to safeguard themselves against the risks involved.

However, certain hard money lenders in California will prefer investors with a strong financial portfolio and credit history by offering favorable loan terms and fairly lower interest rates ranging between 8% and 10% to mitigate the lender’s risks.

#3 Economic Conditions

Real estate markets like California are majorly affected by inflationary pressures and often involve hard money lenders charging higher rates of interest to maintain their profitability positions and secure themselves against any potential risks.

Also, California, being a high-value real estate market, again attracts higher costs of borrowing as it provides various lucrative opportunities to potential borrowers.

However, hard money lenders often struggle with the fears of economic uncertainty, which influences them to take a safer approach by offering higher interest rates , especially in high-demand areas that are quite volatile in nature.

#4 Loan Amount and Term

Hard money loans with a larger amount often involve lower interest rates to attract potential investors easily. However, to mitigate their own risks, hard money lenders may charge origination fees and put across stringent loan terms to reduce the risk of defaults.

These loans involve a shorter timeline, which ranges between 6 months to 24 months, which automatically motivates the lenders to set higher interest rates to maximize their returns in a compressed timeline.

Lenders favor investors with hard-money loan demands because it mitigates their risks and offers them the flexibility to invest in new opportunities easily.

#5 Exit Strategy of the Borrowers

The exit strategy of the potential investors plays a crucial role in deciding the approval of the loan and its terms.

Hard money lenders in California prefer borrowers with a solid exit strategy because these loans are short-term in nature and lenders need the assurance that investors would be able to repay the loan in full, or through refinancing or sale of the property.

Current Hard Money Loan Rates in California

Hard money loan rates in California are fairly higher than traditional loans but have increased marginally as compared to traditional loans, which have tripled in some cases.

These loans typically charge an interest rate that ranges from 9.5% to 12% for 1st position loans and 12% to 14% for 2nd position hard money loans.

Hidden Costs and Fees in Hard Money Lending

Let us explore the various fees and costs that borrowers must look out for while securing a hard money loan:

Fee type

Description

Example

Appraisal Fee

Cost of having the property professionally appraised to assess its market value.

A typical appraisal fee might range from $500 to $1,000.

Legal Fees

Charged for drafting and reviewing the loan documents and agreements.

A lender charges $2,000 in legal fees for document review.

Inspection Fees

Costs for property inspections, often required by the lender before disbursement.

A $300 fee for each property inspection.

Servicing Fee

Ongoing fees for managing and processing loan payments are typically charged monthly.

A $100 monthly fee for a loan serviced over 12 months.

Late Payment Fee

Fee for missing or being late on a scheduled payment.

5% of the monthly payment of $3,000 equals a $150 late fee.

Underwriting Fee

Charged for evaluating the risk of the loan and assessing the borrower’s application.

A lender charges a $1,500 underwriting fee.

Origination Fee

A fee is charged by the lender for processing the loan, usually a percentage of the loan amount.

A 2% origination fee on a $500,000 loan equals $10,000.

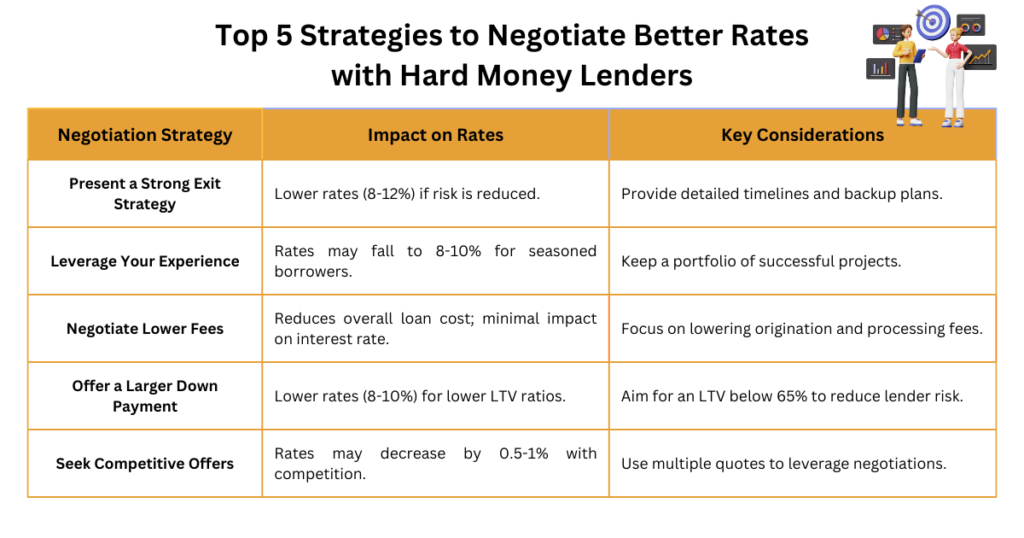

5 Strategies for Negotiating Better Rates with Hard Money Lenders

Top 5 Strategies to Negotiate Better Rates with Hard Money Lenders

Conclusion

California’s high-value market attracts top hard money lenders, offering flexibility and accessibility for investors. As borrowers navigate this competitive landscape, they must consider factors affecting interest rates and clarify all fees to ensure their budgetary needs are met.

Munshi capital provides invaluable support and guidance for both newcomers and seasoned investors. By partnering with experienced professionals at Munshi Capital, investors can secure favorable loan terms and connect with the best money lenders in California, maximizing their long-term investment goals.

Read More: A Complete Guide to Hard Money Lenders in California

Frequently Asked Questions

1. What factors impact the hard money loan interest rate in California?

Factors like lenders’ risk assessment, market conditions, property type, borrowers’ experience, loan-to-value ratio, etc., impact hard money loan rates in California.

2. What are the regulatory considerations for hard money loans in California?

Regulatory consideration for a hard money loan in California includes licensing requirements: a lender should have a license from California Department of Business Oversight (DBO) under the California Finance Lenders Law (CFLL), follow usury law, the borrower should have a Truth in Lending Act (TILA) disclosure, and more.

3. Can I finance multiple properties by using a hard money loan in California?

Yes, a borrower can finance multiple properties using a hard money loan depending on portfolio assessment, LTV consideration, exit strategy, and other related factors.

About the Author

Amish Munshi

I'm Amish Munshi, a mortgage lender with over 20 years of experience in the world of real estate lending. I love breaking down complex loans—like hard money loans, DSCR loans, FHA loans, and other private financing options for real estate—into simple terms so you feel confident at every step of your journey. Whether you're buying your first home or expanding your investment portfolio, I'm here to guide you with the right insights and expertise to help you reach your financial goals.