Hard Money vs. Private Money: What’s the Difference and Which Is Right for You?

Posted on: October 24, 2024

Summary

Introduction Real estate investors with strict timelines and not-so-perfect credit scores often look for quick and flexible financing options. Traditional financing can be daunting due to its stringent approval policies, which can result in prolonged periods. This is where hard money and private money loans can be put into action, offering fast and flexible funding

Real estate investors with strict timelines and not-so-perfect credit scores often look for quick and flexible financing options. Traditional financing can be daunting due to its stringent approval policies, which can result in prolonged periods. This is where hard money and private money loans can be put into action, offering fast and flexible funding to borrowers.

In this blog, we will explain the key distinctions between hard money loans and private money loans and help you decide which is best for your financial goals and needs.

Decoding Hard Money Loans and Private Money Loans

Listed below is a comprehensive overview regarding what are hard money and private money loans:

“What is the difference between a hard money loan and a private money loan”

Hard money or private money? Learn the key differences between these financing options and discover which loan suits your real estate investing needs.

Hard Money Loans

These loans are primarily asset-backed and are secured by the property itself, which eliminates the need to focus on the creditworthiness of the borrower.

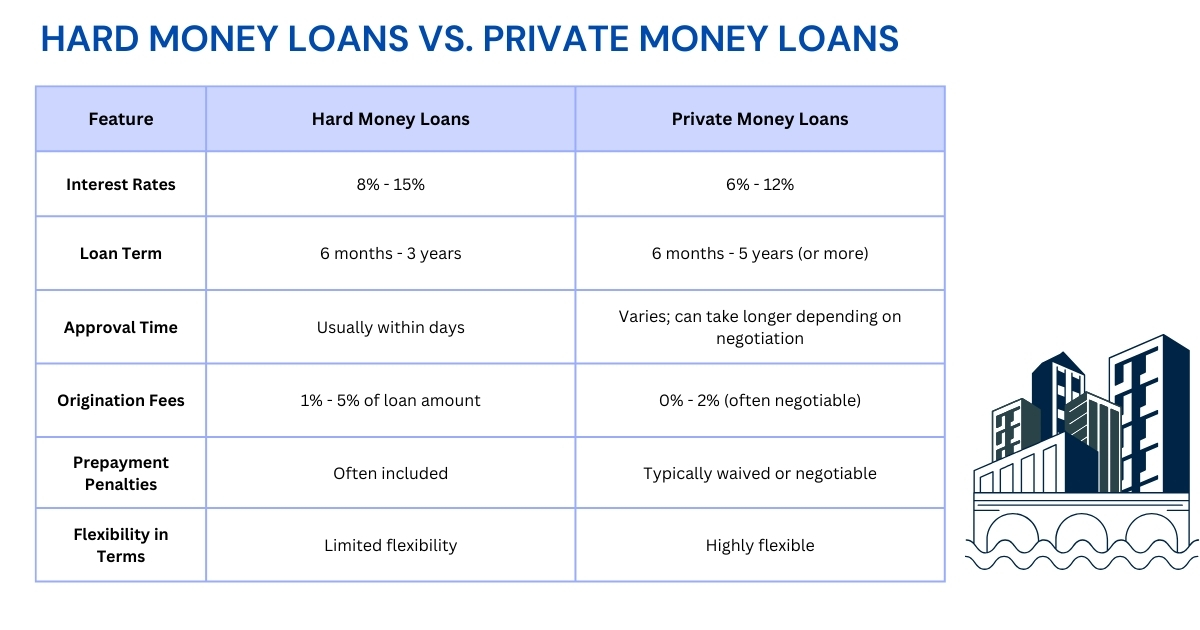

Also, they are short-term in nature, which results in higher interest rates often ranging from 8% to 15% due to increased lender risk.

Hard money loans are usually offered by specialized lending companies for projects that demand quick access to funds for construction, land acquisition, and bridge loans. construction, fix and flip projects, etc.

Relationship-Based Lending: Private money loans are provided by individual investors and are often based on personal and direct connections, fostering trust and flexibility in financing.

Broader Network: While primarily reliant on personal relationships, private money loans can also come from a wider network of individuals, not just those with personal connections.

Flexible Terms: Interest rates and loan terms can vary significantly depending on the relationship between the borrower and lender, often resulting in more favorable conditions for the borrower.

Alternative to Hard Money Loans: These loans are commonly used by borrowers who cannot qualify for traditional financing but seek to avoid the strict terms associated with hard money loans.

What is the Difference in Terms of Use Cases of Hard Money Loan and Private Money Loan?

Hard money loans are not restricted to fix and flip projects; they can also be used in refinancing options, and the same private money loans can be extended to business funding and more.

Loan Type

Common Applications

Hard Money Loans

Fix-and-flip projects, commercial real estate, land acquisition, bridge financing, refinancing options, short-term property investments, distressed properties

Private Money Loans

Smaller, informal loans, larger investments, real estate development, business funding, personal loans based on relationships, flexible short-term financing

What Are The Main Factors To Consider When Choosing Between Hard Money And Private Money Loans?

Selecting between hard money and private money loans is heavily influenced by your investment goals and financial health. Both loans offer quicker access to funds than traditional financing, but they serve different requirements and situations.

Borrowers must consider several key factors before turning to any one of these sources of funding:

Risk Tolerance

Hard money loans lenders engage in stringent repayment terms and higher fees, which may cause a financial burden on the borrower in case any delays are encountered in the investment project.

Private lenders offer understanding and flexibility in loan terms, which is a major advantage in case things go off the track or the timelines are compromised in any manner.

Cost

If cost minimization is your goal, private money lending is the best option for you as it offers lower interest rates, zero or minimal origination fees, and no prepayment penalties.

However, hard money lending can be fast and expensive but with higher interest rates and origination fees along with hefty prepayment penalties.

The decision boils down to whether quick and high-priced hard money loans are justifiable in certain situations.

Your Relationship with Lenders

If you have strong personal connections, private money lending is your savior, as it offers lower cost, flexibility, and easy financing.

If you wish to follow a formal and transactional process to keep yourself in a secure position, hard money lending can provide quicker funds without any dependence on personal connections.

Speed vs. Flexibility

If your major demand is speed and quicker loan approval without any extensive documentation or negotiations, hard money loans are the best option.

If you value flexibility along with tailored loan terms, private money loans are the most viable in the long run.

What Additional Factors Should You Consider When Choosing Between Hard Money and Private Money Loans For Your Real Estate Investment?

Hard money and private money loans are great alternatives for real estate financing but have essential factors, which are discussed as follows:

Loan-to-Value Ratio

Hard money loans lenders are typically offering loan-to-value (LTV) ratios between 60% to 75% of the property’s total value or after-repair value. This means borrowers often need to provide a substantial down payment of 25% to 40%. However, in certain cases, LTV ratios may be extended up to 80% or even 90%, depending on market conditions, the borrower’s financial profile, and the type of property.

Also, these loans are collateral-based, which, when combined with higher LTV ratios, provides significant protection to the lender’s interest in case of any defaults in repayment or the property is sold below its estimated value. They can positively recover their investment.

A higher contribution in the form of a down payment further encourages responsible investment decisions by the borrowers.

Sources of Funds

Hard money lending is usually provided by institutional or semi-institutional private lenders who primarily focus on materializing real estate opportunities.

Their funding mainly comes from specialized lending firms, pooled capital, or investor groups.

Loan from private money lenders are often given to individuals who are a part of their networks or have close connections.

Personal relationships or mutual trust plays a major role in private money lending rather than the borrower’s creditworthiness or financial status.

Private money lenders can be family members, friends, or acquaintances who are willing to offer quick and flexible funding.

Approval Process

Hard money loan approval is primarily collateral-based, which means that borrowers’ credit history and financial well-being are not so essential in comparison to the property’s value.

Hard money lending can be advantageous in the competitive real estate market in securing time-sensitive deals due to less extensive paperwork and fast approval within a matter of days.

The approval process of private money loans is relationship-driven, meaning that the lender may provide funding based on trust or the borrower’s prior performances rather than their credit history or any formal inspections of the property.

This absence of institutional guidelines and independence from perfect credit scores promotes flexible, negotiable, and tailored loan terms.

Flexible Loan Terms

Private mortgage lenders typically offer more flexible and negotiable loan durations compared to hard money lenders. Since private lenders are not bound by institutional guidelines, they can tailor loan periods based on their relationship with the borrower

In contrast, hard money lenders usually provide non-negotiable short-duration funding to mitigate their increased risk and recoup their investment. However, some hard money lenders may also be open to flexible terms, including extending loan durations, depending on the borrower’s experience and the strength of their relationship with the lender.

Interest Rates and Fees

Private lenders for real estate offer loans at interest rates ranging between 6% and 12%, which can be negotiated for lower rates by borrowers who share strong relations with the lender. Additionally, the interest rates on private money loans can vary significantly, influenced by the nature of the relationship and the individual preferences of the lender.

Hard money loans are provided at higher interest rates ranging between 8% to 15% to secure the lender’s interest.

Private lending usually attracts quite low origination fees, typically between 0% to 2% or in some cases, no fees at all. However, hard money loans involve higher origination fees, which range from 1% to 5%.

What are the Risk Considerations for Lenders in Hard Money Loans vs Private Money Loans?

Listed below are the various considerations to be taken into account for hard money or private lending:

Risk Factor

Hard Money Loans

Private Money Loans

Default Risk

Higher due to distressed properties or poor credit

High if based on personal relationships, not formalized

Collateral Security

Secured by real estate, reducing some risk

May or may not be secured by assets, increasing risk

Regulatory Compliance

Subject to strict regulations (e.g., TILA, usury laws)

Less regulated, but still subject to local usury laws

Market Risk

Vulnerable to property market fluctuations

Similar market risks if real estate is involved

Conclusion

While private money loans offer flexible, individualized funding based on personal ties, It allow rapid access to finance but frequently have severe terms. Choosing the right option depends on your specific financial needs and goals. Munshi capital simplifies the process by offering tailored, fast approval and quick funding solutions, empowering both seasoned investors and newcomers to pursue real estate projects with confidence.

Read More: How To Secure A Hard Money Loan With A Low Credit Score? – Munshi.captal

Frequently Asked Questions

Are there any prepayment penalties in hard money and private money loans?

Yes, hard money lending involves prepayment penalties between 1% to 5% while private money loans have zero to minimal penalties between 0% to 2%.

What is the LTV ratio offered by hard money loans California?

Most of the hard money lenders in California offer loan-to-value ratios between 60% to 80% or higher in the case of experienced investors or low-risk projects.

Are hard money loan rates negotiable in California?

Yes, hard money loan rates in California can be negotiated if the borrowers have a solid credit portfolio or are willing to contribute a hefty down payment as their equity in the investment.

What are the regulatory differences between hard money loans and private money loans?

Hard money loans are regulated, requiring lender licensing, compliance with usury laws, and strict disclosures. Private money loans are less regulated with flexible terms but must adhere to local usury laws.

Can hard money loans be used as a short-term financing option for refinancing later?

Yes, it can be used as a short-term financing alternative for faster acquisitions, and they can be refinanced into conventional loans once the property’s financial situation improves or stabilizes.

About the Author

Amish Munshi

I'm Amish Munshi, a mortgage lender with over 20 years of experience in the world of real estate lending. I love breaking down complex loans—like hard money loans, DSCR loans, FHA loans, and other private financing options for real estate—into simple terms so you feel confident at every step of your journey. Whether you're buying your first home or expanding your investment portfolio, I'm here to guide you with the right insights and expertise to help you reach your financial goals.