How Do I Qualify for a DSCR Loan for My Airbnb or Short-Term Rental?

Posted on: October 16, 2024

Summary

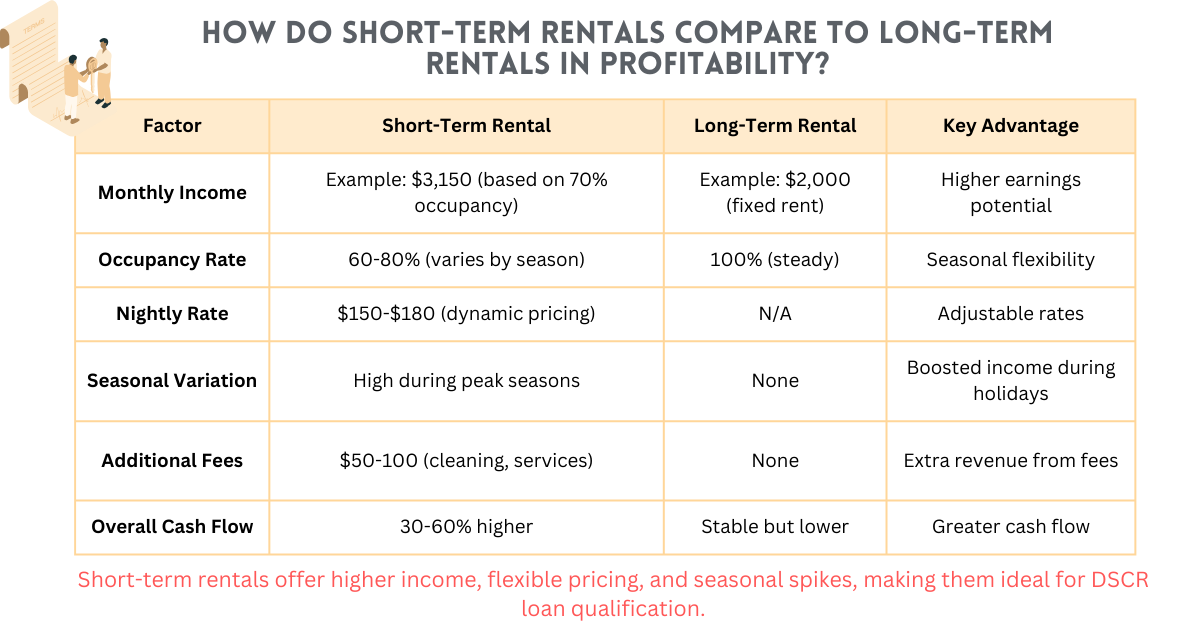

The short-term vacation rental market, valued at $109.76 billion in 2022, is projected to grow by 11% annually through 2030, attracting real estate investors to properties like Airbnbs. To finance these investments, DSCR (Debt Service Coverage Ratio) loans are an excellent option, offering flexibility and favorable terms. This guide explores how DSCR loans work, the qualification process, required documents, and key factors for choosing a lender, making it the perfect solution for Airbnb and short-term rental investments.

.svg)

.svg)