Living in a high-cost area, like California, often requires taking out a jumbo loan to finance your home. But what happens when refinance jumbo loan rates drop, or your financial situation improves? Jumbo loan refinancing can be a great way to reduce costs and adjust your mortgage to better suit your needs. However, refinancing a jumbo loan isn’t for everyone, so it’s important to understand the nuances before diving in.

Why Should You Refinance Your Jumbo Loan?

Refinancing a jumbo loan can be an excellent strategy for homeowners looking to save money or adjust the terms of their loan.

Here are the top reasons why you might want to consider a jumbo loan refinance:

#1 Lower Interest Rates:

One of the most common reasons for jumbo loan refinancing is to take advantage of lower interest rates. By securing a lower rate, you could significantly reduce your monthly payments and save thousands over the life of the loan.

Tip: Use a mortgage calculator to assess how much you could potentially save by refinancing jumbo loans.

#2 Cash-Out Refinance:

A jumbo cash-out refinance allows you to tap into the equity you’ve built in your home. This can be useful for covering home improvements, consolidating debt, or even funding other investments. Keep in mind, though, this will increase your loan balance and may affect your interest rate.

Tip: Consider this option if you need funds for major expenses and have enough equity built up

#3 Improved Loan Terms:

Jumbo loan refinancing can also help you adjust the terms of your loan. For example, you may want to switch from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage for more stable payments or shorten the loan term to pay off your home faster.

Tip: If your financial situation has improved, consider a shorter loan term to save on long-term interest.

Benefits of Jumbo Mortgage Refinancing

Refinancing your jumbo mortgage offers several key advantages:

- Lower Monthly Payments

By securing a lower interest rate, you can significantly reduce your monthly mortgage payments, freeing up more cash flow for other expenses or investments.

- Cash-Out Options

Tap into the equity you’ve built in your home with a jumbo cash-out refinance, allowing you to fund home improvements, consolidate debts, or invest in new opportunities.

- Improved Loan Terms

Switch from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage (FRM) for more predictable payments or shorten your loan term to pay off your mortgage faster and save on long-term interest.

- Better Interest Rates

If refinance jumbo loan rates are lower now than when you initially took out the loan, you can save thousands over the life of the mortgage by locking in a better rate.

Now that we’ve outlined the benefits, let’s dive into how to approach jumbo loan refinancing.

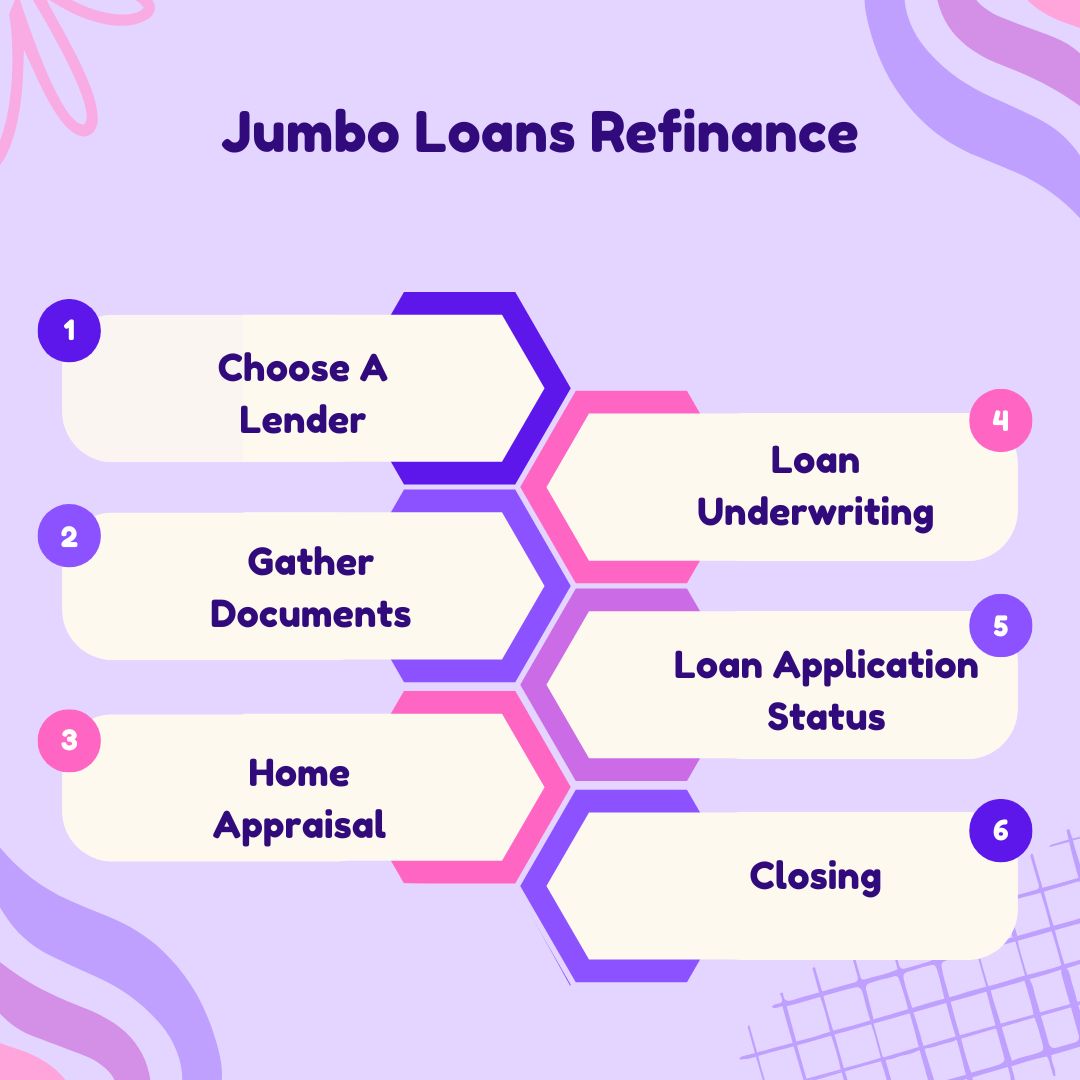

6 Easy Steps For Jumbo Loan Refinance

Refinancing a jumbo loan involves several steps that mirror those of a conventional refinance. Here’s how the process works:

Here’s a detailed procedure for the jumbo loan refinance process:

Step 1: Choose a Lender

Before deciding to stay with your current lender, it’s a good idea to compare different lenders. Jumbo loan refinancing comes with stricter requirements, so shopping around can help you find better refinance jumbo rates and terms.

- Current Lender: Reach out to your existing lender to see if they can offer a competitive jumbo loan refinance package.

- New Lender: If your current lender doesn’t offer favorable terms, compare other lenders that specialize in refinancing jumbo loans.

Tip: Look for lenders that offer jumbo-specific refinancing options to ensure you’re getting the best deal.

Step 2: Gather Documents

As with any loan process, you’ll need to provide detailed documentation to prove your financial standing. Some common documents include:

- Tax returns

- Recent bank statements

- Pay stubs

- Proof of income

Tip: Ensure all documents are up-to-date and accurate to streamline the application process.

Step 3: Home Appraisal

Your lender will require a home appraisal to determine the current market value of your property. This step is crucial because it establishes how much equity you have in your home, which will affect your jumbo cash-out refinance options.

- Lender arranges appraisal: A professional appraiser will visit your home and assess its value based on market conditions and the property’s condition.

Tip: Make sure your home is in good condition before the appraisal to maximize your property’s value.

Step 4: Loan Underwriting

Once the appraisal is complete, the lender will begin the underwriting process to assess the risk of refinancing your jumbo loan. Underwriting for jumbo loans is often more rigorous and may involve manual underwriting. Unlike automated systems used in conventional loans, manual underwriting requires a financial expert to carefully review your income, assets, credit history, and other details. While this process is more thorough, it can also be time-consuming.

- Credit check: Ensure your credit score remains steady throughout this process by avoiding new debts or large purchases.

Tip: Stay on top of your finances during underwriting to prevent any surprises that could delay the jumbo loan refinance.

Step 5: Loan Application Status

After underwriting, your lender will either approve or deny your application. If approved, you can proceed with the closing process.

- Closing costs: Be prepared to pay closing costs, which usually range from 2% to 6% of the loan amount. For jumbo loans, closing costs tend to be higher due to the larger principal balances. For instance, on a $1 million jumbo loan, closing costs could range from $30,000 to $60,000. Some lenders may offer the option to roll these costs into the loan, increasing your loan balance but reducing the upfront cash requirement.

Tip: If your application is denied, work on improving your financial standing before reapplying.

Step 6: Closing

Once you’ve closed on the refinance, you’ll have a new mortgage with updated terms, whether that’s a lower interest rate, a new loan term, or a fixed-rate structure. Congratulations — you’ve successfully refinanced your jumbo loan!

Following these six steps ensures a smooth and efficient jumbo loan refinance process, helping you secure better terms for your mortgage.

Qualification For Refinancing A Jumbo Loan

Refinancing a jumbo loan has stricter requirements compared to other types of loans. Here’s how you can qualify:

- Credit Score:

- Minimum Scores: For a 30-year fixed-rate jumbo loan refinance, you’ll need a credit score of at least 680. For 15-year fixed loans or adjustable-rate mortgages (ARMs), you might need a score of 700 or higher.

- Tip: If refinancing an investment or rental property, expect to need a credit score closer to 760.

- Debt-To-Income Ratio (DTI):

- Your DTI represents the percentage of your income that goes toward debt payments. Most lenders require a DTI below 43%, though stricter lenders might expect a DTI of 36% or lower for jumbo loan refinancing.

- Payment History:

- Having a clean payment history is essential. If you’ve missed payments or recently declared bankruptcy, it’s unlikely you’ll qualify for refinancing your jumbo loan.

- Home Equity:

- Lenders typically require you to maintain 20% to 30% equity in your home after jumbo loan refinancing. This is especially important if you’re considering a jumbo cash-out refinance.

- Liquid Reserves:

- Lenders want to see that you have liquid assets or cash reserves available to cover several months of mortgage payments, just in case of financial hardship.

Is Refinancing a Jumbo Loan Right for You?

Before you proceed with jumbo loan refinancing, ask yourself the following:

- Are refinance jumbo loan rates significantly lower?

A drop in rates by 0.5% to 1% could make refinancing a jumbo loan worthwhile, even with closing costs.

- Can you meet the financial requirements?

Make sure your credit score, DTI, and cash reserves are in good shape before starting the refinance process.

- Do you plan to stay in your home long term?

If you’re near the end of your loan term, refinancing your jumbo loan might not save you much in interest over time.

How To Find Lender To Refinance A Jumbo Loan?

Not all lenders offer jumbo loan refinancing, so it’s important to do your research. Look for reputable lenders who specialize in refinancing jumbo loans and offer competitive rates. Compare their fees, closing costs, and customer reviews to make an informed decision.

Tips for Finding a Lender:

- Compare multiple offers: Don’t settle for the first lender. Compare rates and terms from at least three different providers.

- Inquire about special programs: Some lenders may offer special programs or incentives for refinancing jumbo loans.

- Prioritize customer service: Since jumbo loans are more complex, choose a lender known for excellent customer service.

The Bottom Line

So, you’ve learned about jumbo loan refinancing and how it can potentially save you money on your mortgage. But how do you know if it’s the right move for you?

Here’s the deal: Refinancing can lower your interest rate and monthly payment, but there are upfront costs involved. It’s a good idea to chat with a qualified lender to see if the numbers work out in your favor.

Ready to find out? Contact me to help you explore your options and see if jumbo loan refinancing makes sense for your situation. I’ll walk you through the process and answer any questions you have in easy-to-understand terms.

.svg)

.svg)