No-Doc Home Loans for Primary Residences: A Guide for Borrowers

Posted on: September 17, 2024

Summary

No-doc home loans, or no income verification loans, are designed for self-employed individuals or those with irregular income who cannot provide traditional income proof. These loans offer flexibility but come with higher interest rates, stronger credit score requirements, and larger down payments to mitigate risk. Types include NINA (No Income, No Assets) and SIVA (Stated Income, Verified Assets). Munshi Capital offers tailored mortgage options to meet borrowers’ unique financial needs and goals.

No-Doc home loans are loans that do not require any income verification of the potential borrowers. These are sometimes also referred to as NINJA loans, which stand for no income, no job, and no assets.Before the global financial crisis in 2008, no-doc home loans held a substantial part of approximately 40% of the subprime mortgages by 2006. These loans are still alive in the real estate market for individuals with subprime incomes and low credit scores. However, only3% of lenders are presently offering no income mortgage loans and they may ask the borrowers to have certain documents, such as tax returns, bank statements, etc., to verify the genuineness of the borrower’s income. The blog will cover all different aspects of no-doc home loans for borrowers to understand and evaluate the loan option.

What are No-Doc Home loans?

No-Doc home loans, also known as no income verification home loans, engage with those borrowers who are unable to furnish traditional income verification documents. The lenders of these no income check mortgage loans deduce potential borrowers’s eligibility based on their repayment capacity, credit score, and possession of assets. These loans are best suited for individuals with not-so-consistent streams of income. To eliminate and secure themselves from the risks involved, lenders may charge higher interest rates to the borrowers. Let us understand the key characteristics of no doc home loans with the example given below:

Aspect

Example Scenario

Key Characteristics

Loan Type

No-Doc Loan

Suitable for non-conventional borrowers.

Income

Presents an income of $100,000 (no proof needed).

No stringency for borrowers to furnish traditional income sources.

Employment

Freelancer

Overall flexibility for self-employed individuals.

Interest rate

7 % or higher

Lenders secure themselves against potential risks of the mortgage without income verification.

Credit Score

700 or higher

Higher credit score to safeguard against risks.

Down payment

20% or more

A substantial down payment is a prerequisite to reduce the lender’s involvement.

Assets

$370,000 in savings

A substantial show of liquid assets reflects a strong financial portfolio of the borrowers.

Types of No-Doc Home Loans

No-doc home loans are further subdivided into various types based on asset and income verification, which are as follows:

No Income, No Assets (NINA): These no-doc home loans are suitable for borrowers who prefer minimal documentation with no income or asset verification.

No Income, Verified Asset (NIVA): These are no income check mortgage home loans that involve verification of the property involved but the borrower’s inability to establish their income properly.

Stated Income, Verified Asset (SIVA): These no-doc home loans require the borrowers to divulge their proof of income without any comprehensive documentation but with the prerequisite of asset verification.

Stated Income, Stated Asset (SISA): These types of no-doc home loans are easier to approach because they require a declaration of income as well as the asset but without any intricate documentation.

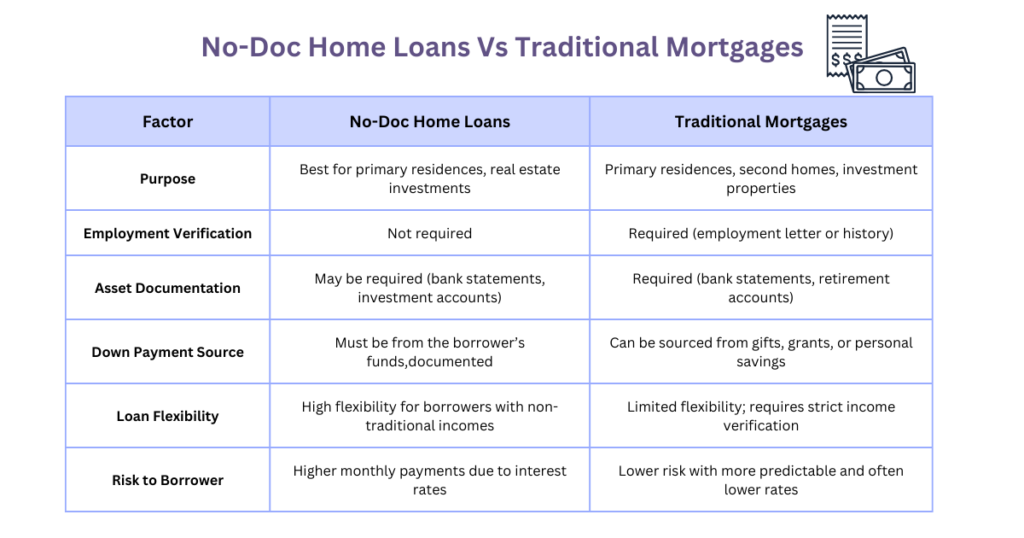

“No Doc Home Loans vs. Traditional Mortgages or Loans”Discover the process of securing a no-doc home loan and how these can be tailored to your personal needs and financial goals.

Steps to Apply for a No-Doc Home Loan

Borrowers must understand the below-given five basic steps to successfully apply for a no-doc home loan:

Step 1: Improving Financial Situation: Potential borrowers must focus on elevating their financial portfolio, like having a good credit score, substantial liquid assets, etc., before applying for a no-doc home loan.

Step 2: Considering Loan and Lender Options: Borrowers must search for lenders who specialize in no-doc home loans and offer flexible loan options too.

Step 3: Gather Necessary Documentation: Although no-doc home loans do not require conventional documentation, borrowers must produce certain documents to confirm their financial stability.

Step 4: Finalize your Loan Application: After choosing the right lender and furnishing the basic documentation, borrowers must submit their loan application at the earliest to ensure faster approval.

Step 5: Closing the Deal: After all the basic requirements are fulfilled, lenders will finalize the loan approval, and the application will be considered closed.

Pros of No-Doc Home Loans

No-doc home loans are a type of no verification mortgage loan that presents various advantages for borrowers, especially the ones who are not willing to engage in any complex documentation. Let us discuss these advantages:

Financial flexibility: Because of its emphasis on minimal income paperwork, no-doc home loans are an excellent choice for borrowers seeking quick access to capital funding. This further promotes the preservation of liquid funds of the potential borrowers.

Flexible loan terms: No-doc home loans are a great option for borrowers who demand flexible terms of financing based on their financial portfolio and credit history.

Savior for non-traditional income borrowers: These low doc mortgage loans are a boon for non-traditional and self-employed borrowers who are unable to present their evidence of income to conventional lenders.

The optimal choice for high-net-worth individuals: These wealthy borrowers can take advantage of their solid asset background and perfect credit scores to secure a no-doc home loan that best suits their specific requirements.

Streamlining application process: One of the major pros of these no-verification mortgage loans is that extensive documentation is not essential for securing these loans. This boosts faster and easier loan approval with shortened closing times.

Conclusion

Navigating the market of residential financing can be difficult, especially for borrowers who have irregular income sources. No-doc home loans are a great alternative to traditional financing which can be quite challenging to secure for borrowers with unique financial needs. However, these loans come with the drawbacks of higher interest rates, larger down payments, and strong credit scores, which are essential to securing these loans to mitigate the lender’s risks. These challenges must be taken into account by the borrowers before indulging in the market of no-doc home loans.Borrowers can take the advantage of personalized conventional mortgages offered by Munshi. Capital to get advantage of customized loan options and fulfill your homeownership dreams that support their unique needs and long-term financial goals.Read More: Home loan without W2, Pay Stubs or Tax returns

Frequently Asked Questions

#1 How can borrowers benefit from no-doc home loans when working with professionals like Munshi Capital?Borrowers are provided with access to expert guidance, customized solutions, and genuine lenders to easily streamline the financing process.#2 Can a no-doc home loan be used to invest in the real estate market?Yes, borrowers can use no-doc financing to invest in the real estate market.#3 If I am a self-employed individual, can I apply for no doc home loans?Yes, self-employed individuals can apply for a no-doc home loan subject to meeting good credit and substantial down payment requirements.#4 What are the underwriting criteria for no doc home loans?For a no-doc home loan underwriting criteria involves credit scrutiny, property analysis, asset-based assessment, etc.

About the Author

Amish Munshi

I'm Amish Munshi, a mortgage lender with over 20 years of experience in the world of real estate lending. I love breaking down complex loans—like hard money loans, DSCR loans, FHA loans, and other private financing options for real estate—into simple terms so you feel confident at every step of your journey. Whether you're buying your first home or expanding your investment portfolio, I'm here to guide you with the right insights and expertise to help you reach your financial goals.