The Ultimate Guide to FHA Construction Loans: How to Build Your Dream Home

Posted on: September 13, 2024

Summary

FHA construction loans are a flexible, government-backed financing option designed for borrowers with low credit scores or minimal down payments, offering a streamlined process to fund both the construction and permanent mortgage under a single loan structure. In 2024, FHA loan limits range from $498,257 to $1,149,835, with higher limits for more expensive areas. These loans, including the FHA 203(k) for renovations and the one-time close construction loan for building from scratch, simplify homeownership by minimizing paperwork and reducing upfront costs. Eligibility criteria include a credit score of 580 or above, a debt-to-income ratio below 50%, and a two-year employment history. Borrowers benefit from low down payments, easier credit requirements, and government-backed security. Munshi Capital ensures a smooth loan process by connecting borrowers with certified lenders and builders, aligning their financing with long-term financial goals.

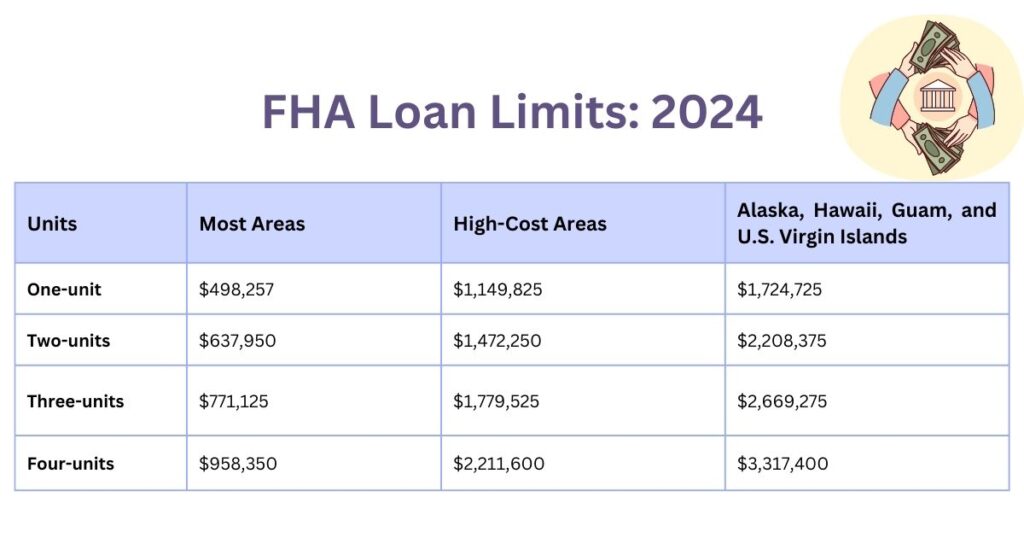

A FHA construction loan is a great financing option for borrowers, especially those with a low credit score and lower down payments who wish to build their dream home from scratch. These loans have become quite popular in the market due to their easy availability while offering a single loan structure combining construction and permanent mortgages. As a result, in 2024, FHA loan limits are ranged between $498,257 to $1,149,835. These limits can be higher for expensive areas outside the continental U.S.The single loan structure in FHA construction loans minimizes the hassle of extra paperwork and additional costs, further promoting an easy financial process. With flexibility and accessibility as key features, an FHA construction loan is the most favorable option for acquiring convenient homeownership.

What are FHA Construction Loans?

FHA construction loans are mortgages backed by the government to build a new property or refurbish an existing one. Unlike traditional loans, which provide for the costs involved in an already finished property, FHA construction loans offer the benefit of funding the construction costs as well as delivering a permanent mortgage once the construction is complete, thus proposing a single all-inclusive loan.These loans are insured by the Federal Housing Administration (FHA), a branch of the United States Department of Housing and Urban Development (HUD), thus automatically attracting first-time home buyers as well as minimizing the lender’s risk and offering flexible financing options to borrowers with a low credit score and lesser down payments.

FHA Construction Loans: Different Types

FHA construction loans are further subdivided into two types, which are discussed below:

FHA 203(k) loan: This loan is often used for acquiring properties demanding repairs or renovations, thus combining the features of purchasing and renovating in a single loan.

These are again further divided into two types: the Standard 203(k) for major construction projects and the Limited 203(k) for smaller-scale renovations.

FHA one-time close construction loan: This loan integrates the financing of the purchasing and construction aspects in a single loan, which helps the borrowers build their dream homes from scratch. It also eliminates the need for excessive paperwork, extra costs, and the hassle of streamlining two separate loans.

Eligibility Criteria: FHA Construction Loans

FHA construction loans are relatively flexible to process as compared to traditional loans, but the applicants need to meet certain criteria, which are discussed below:

FHA loan limits: Borrowers should double-check their county’s limits before applying for an FHA construction loan because they vary by county across the United States and are also influenced by the local market conditions.

Learn how FHA construction loans can help you build your dream home. Explore eligibility criteria, loan limits, credit score requirements, and other key aspects.

“FHA 2024 loan limits”

Debt-to-Income ratio: This ratio examines the borrower’s monthly payments to their income. A DTI below 50% is considered acceptable, but certain lenders may approve a higher DTI due to the borrower’s overall sound financial portfolio.

Employment and income verification: Such lenders only approve borrowers who have furnished genuine proof of at least two years of stable employment and income details.

Credit Score: These loans require a credit score of 580 or above with an initial compulsory down payment of 3.5%, but certain borrowers with a credit score between 500 and 579 may also get approved, attracting a higher down payment of up to 10%.

Occupancy: The main goal of these loans is to build a home for their borrowers, and it must be occupied within 60 days of closing the deal.

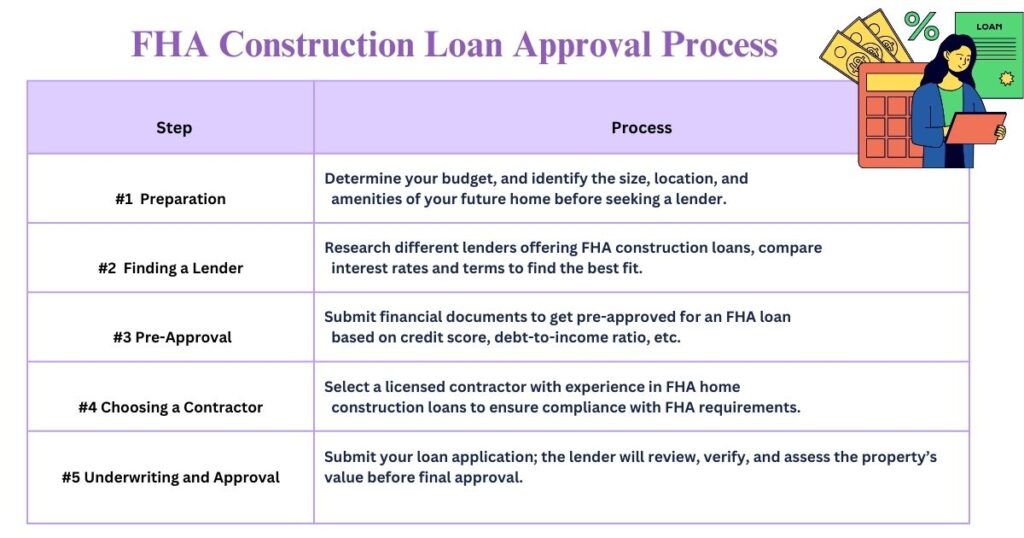

“ FHA construction loan approval process”

Benefits of FHA construction loans

FHA construction loans offer various advantages that may help in attracting potential borrowers, especially the ones who were not eligible for traditional loans:

Government-supported security: These loans are supported by the Federal Housing Administration, which encourages lenders to offer debt at favorable terms, even to borrowers with a higher risk profile.

Lower down payment: These loans do not burden the borrowers with a hefty down payment by offering rates as low as 3.5%.

Single loan structure: The feature of streamlining purchase and construction loans in a single loan simplifies the overall process and eliminates interest rate fluctuations associated with individual construction and permanent loans.

Easier credit guidelines: These loans have easier credit prerequisites, encouraging borrowers even with a weak credit profile to build their dream homes who might face challenges in applying for traditional loans.

Conclusion

FHA construction loans are easier and more accessible financing options for potential borrowers who may have struggled with a weak financial portfolio. However, the path to securing these loans comes with its challenges. These loans involve a more complex procedure when compared to traditional loans. Despite the obstacles, the advantages often have an edge over the disadvantages.Working with professionals like Munshi Capital ensures that borrowers have an effortless experience in navigating this process. They provide the necessary guidance and support to borrowers to successfully connect with certified lenders and builders, while also focusing that these loans are in synchronicity with their long-term financial goals and lifestyle choices.Read More: FHA Construction Loan Down Payment

Frequently asked questions

1. How to get faster approval for FHA construction loans?Borrowers must prioritize decreasing their debt-to-income ratio and improving their credit score to 580 or above.2. What if the cost of construction is more than the loan amount?The borrower will be accountable to fulfill the exceeded amount to complete the construction process.3. Can borrowers use FHA loans to purchase land?Yes, borrowers can buy the land itself or can do both purchase and construction on the acquired property.

About the Author

Amish Munshi

I'm Amish Munshi, a mortgage lender with over 20 years of experience in the world of real estate lending. I love breaking down complex loans—like hard money loans, DSCR loans, FHA loans, and other private financing options for real estate—into simple terms so you feel confident at every step of your journey. Whether you're buying your first home or expanding your investment portfolio, I'm here to guide you with the right insights and expertise to help you reach your financial goals.