Address: 3255 Ashbourne Cir San Ramon CA 94583

Call: 877-343-7379

Email: info@munshi.biz

We value your time

Learn the secrets of mortgage world and save on your most expensive budget item!

Eager to know more on how to save on your mortgage?

join us to learn more

Information you were waiting for is available right here! From first time home buyers to seasoned investor and fund managers rely on this information to make informed decisions about their real estate financing.

Hard Money Lenders in 2026: The Strategic Investor’s Guide to Private Capital

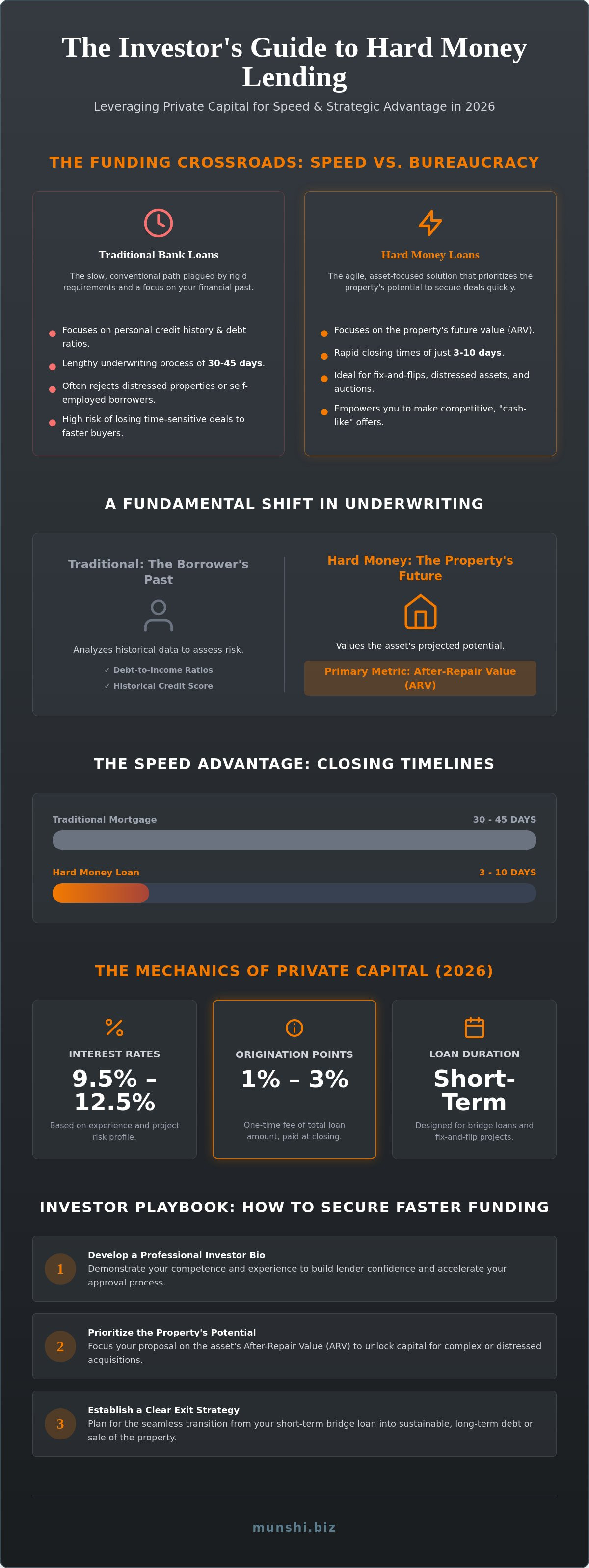

In the high-velocity real estate market of 2026, speed is no longer a luxury; it's the primary currency of the successful investor. You've likely watched a prime opportunity slip away while waiting for a traditional bank's underwriting department to process a mountain of paperwork. It's frustrating to lose a deal because of rigid institutional requirements that don't account for your unique situation as a self-employed borrower or the potential of a distressed property. Many sophisticated investors now rely on hard money lenders to bypass these hurdles and secure assets before the competition can even schedule an appraisal.

This guide will show you how to master the mechanics of private capital and leverage the agility of asset-based lending to scale your portfolio with surgical precision. You'll learn to move beyond the constraints of traditional finance by focusing on the intrinsic value of the property rather than just your personal credit score. We will break down the current cost of capital, explore the shift toward fundamental value, and explain how to establish a reliable partnership that fuels your long-term growth. By the end of this article, you'll have a clear roadmap for securing fast, reliable funding that keeps your investment strategy moving forward with confidence and clarity.

Key Takeaways

- Identify how asset-based financing prioritizes property value over personal credit to unlock capital for complex real estate acquisitions.

- Master the 2026 lending environment by identifying how hard money lenders structure rates and terms for maximum tactical agility.

- Compare private capital against traditional mortgages to ensure you deploy the most effective financing tool for time-sensitive deals or distressed assets.

- Accelerate your approval process by developing a professional Investor Bio that demonstrates competence and secures faster funding commitments.

- Establish a strategic partnership to facilitate the seamless transition from short-term bridge loans into sustainable long-term debt structures.

What Are Hard Money Lenders and Why Do Strategic Investors Use Them?

Hard money lenders operate as private entities that offer short-term, asset-backed financing to real estate professionals. While institutional banks prioritize a borrower's personal financial history, these lenders focus on the intrinsic value of the real estate asset serving as collateral. Hard money is a strategic tool for liquidity in real estate that enables investors to capture high-value opportunities requiring immediate capital deployment. In the 2026 real estate landscape, where inventory remains historically low and competition for distressed assets is fierce, private capital has transitioned from a niche alternative to an essential facilitator for portfolio growth.

The Core Difference: Asset-Based vs. Credit-Based Underwriting

Traditional underwriting is fundamentally a look into the past. It relies on debt-to-income ratios and historical credit scores to determine risk. Hard money lenders adopt a more visionary approach by focusing on the After-Repair Value (ARV) of the property. This collateral-focused methodology allows for the successful funding of distressed properties that banks would otherwise reject due to their current condition. By 2026, the industry has seen a significant shift toward more sophisticated risk-modeling. Lenders now utilize advanced data analytics to project property performance with remarkable accuracy. This ensures that the viability of the project remains the primary driver of the lending decision, providing a path for self-employed borrowers who may have complex tax returns but significant equity and experience.

Speed as a Competitive Advantage

In a market where timing is everything, speed becomes your most potent competitive advantage. Traditional mortgage approvals often take 30 to 45 days. This timeline is frequently incompatible with the needs of a modern investor. Private capital providers can often close in as little as 3 to 10 days, providing the tactical agility needed to secure time-sensitive assets. This rapid turnaround allows you to present "cash-like" offers that carry significant weight in competitive bidding scenarios. Whether you are targeting off-market deals, participating in high-stakes foreclosure auctions, or looking to bridge a gap between projects, the efficiency of hard money loan structures gives you the ability to move with purpose. This speed does more than just help you win deals; it builds your reputation as a reliable closer among brokers and sellers alike.

The Mechanics of Private Capital: Terms, Rates, and 2026 Market Realities

Efficiency in private lending is built on a clear understanding of the financial structure. Strategic investors don't view interest as a debt burden; they treat it as a cost of goods sold. This mental shift allows you to focus on the net profit of a deal rather than the nominal rate. In 2026, hard money lenders have refined their models to offer more personalized structures, but the core components remain consistent. A recent Forbes analysis of hard money lenders highlights that while these rates are higher than conventional debt, the speed of execution often outweighs the incremental cost. Transparency has become the industry standard. Professional facilitators now provide clear term sheets that eliminate hidden fees, ensuring you can calculate your exact ROI before signing.

The 2026 economic landscape is characterized by a return to fundamentals. As traditional banks maintain tight underwriting standards, the demand for fast, flexible capital has surged. This has led to a more competitive private lending environment where experienced borrowers can secure more favorable terms. Identifying a partner who offers transparent Bridge Loans or fix-and-flip financing is essential for maintaining your competitive edge in a low-inventory market.

Interest Rates and Points: Calculating the Total Cost

The anatomy of a private money deal typically involves two primary costs: the interest rate and origination fees, commonly known as "points." In the current 2026 market, interest rates generally range from 9.5% to 12.5%, depending on your experience level and the project's risk profile. Points typically fall between 1% and 3% of the total loan amount. These are one-time fees paid at closing that impact your initial capital outlay. Most loan durations are short-term, spanning 6 to 24 months. This duration is perfectly suited for bridge scenarios where you intend to stabilize an asset and then transition into long-term debt or sell the property for a profit.

Loan-to-Value (LTV) and After-Repair Value (ARV)

Lenders use Loan-to-Value (LTV) and After-Repair Value (ARV) to manage risk and determine the maximum loan amount. Most hard money lenders provide between 60% and 75% of the property's current value. For renovation projects, ARV-based lending is the superior choice. This allows you to borrow based on what the property will be worth after improvements are completed. Some lenders may even cover up to 95% of the loan-to-cost (LTC) for highly experienced investors. Accurate appraisals are the cornerstone of this process. They protect both the lender and the borrower from market volatility by ensuring the project is grounded in realistic financial expectations. When you understand these mechanics, you can move from a transactional mindset to a strategic one, using capital as a precise tool for growth.

Hard Money vs. Traditional Financing: A Strategic Comparison

Choosing between private capital and institutional debt isn't a matter of preference; it's a tactical decision based on your project's lifecycle. Traditional lenders excel at providing low-cost, long-term capital for stabilized assets. Hard money lenders, by contrast, provide the high-velocity funding required to secure and renovate properties that don't yet meet institutional standards. A strategic investor understands that these two financing types are not mutually exclusive. Instead, they represent different phases of a sophisticated investment strategy. You might use a bridge loan to acquire a distressed asset and then transition into Conventional Loans or DSCR Loans once the property is stabilized and cash-flowing. This "proactive partnership" model ensures you always have the right capital structure for your current objective.

The primary differentiators between these paths are documentation and property condition. Banks require exhaustive proof of personal income and properties that are immediately habitable. Private capital focuses on the deal's potential. This allows you to bypass the 45-day waiting period and the rigid debt-to-income requirements that often stall self-employed professionals. By aligning with a facilitator who understands both private and traditional markets, you gain the agility to pivot as your portfolio matures.

When to Choose Private Capital

- Fix-and-flip projects: When speed and renovation funding are paramount to your ROI.

- Distressed acquisitions: Properties that lack "habitable" status and are ineligible for FHA or conventional financing.

- Complex borrower profiles: High-net-worth individuals with sophisticated tax structures that traditional underwriters struggle to interpret.

- Competitive bidding: Scenarios where a 5-day closing is the only way to win an off-market deal.

When to Stick with Conventional Loans

Conventional financing remains the gold standard for long-term stability. If you're purchasing a primary residence or a turnkey rental property that already meets all safety and structural standards, the lower interest rates of traditional debt are unbeatable. These loans are designed for the "hold" phase of your strategy, where minimizing monthly interest expense is the primary goal. While hard money lenders provide the fuel for growth, FHA Loans and conventional mortgages provide the foundation for long-term wealth preservation. Understanding when to switch from one to the other is what separates a transactional flipper from a visionary fund manager. You don't need to choose one path forever; you simply need the right partner to guide you through each transition.

The Path to Funding: How to Qualify and Secure Your Deal

Securing capital from hard money lenders is a professional exchange of value rather than an institutional interrogation. While traditional banks focus on your historical tax returns, private capital focuses squarely on your ability to execute a specific vision. Success in this arena requires more than just a promising property; it requires a demonstrated level of competence. This starts with your Investor Bio. This document functions as a professional resume that highlights your track record, your core team of contractors, and your history of successful exits. By presenting yourself as a seasoned operator, you reduce the perceived risk for the lender and often unlock more favorable terms. Precision in your presentation signals that you are a partner worth investing in.

The Application Checklist for 2026

While the documentation is significantly less burdensome than a conventional mortgage, it is far from non-existent. In 2026, efficiency is driven by digital transparency and rapid verification. You'll need to provide several key documents to move through underwriting at pace:

- A signed purchase contract: This establishes the legal basis for the entire transaction.

- A detailed Scope of Work (SOW): A line-item budget that proves you understand the renovation requirements and material costs.

- Proof of liquidity: Verification that you have the "skin in the game" required for down payments, closing costs, and interest reserves.

- A realistic project timeline: A schedule that accounts for current permitting speeds and local labor availability.

Lenders prioritize borrowers who can show a history of successful projects, as experience is the most reliable predictor of project completion. If you're a first-time investor, partnering with an experienced contractor can bridge the gap in your bio and provide the necessary assurance to your funding partner.

Developing a Robust Exit Strategy

The most critical element of your proposal is the exit strategy. Hard money lenders are short-term partners; they want to see exactly how their capital will be returned. A deal without a clear exit is simply a risk without a map. Your primary exit is typically selling the property for a profit. This requires a rigorous market analysis of comparable sales to justify your projected After-Repair Value. However, many sophisticated investors in 2026 utilize the BRRRR method. This involves transitioning from short-term capital into long-term debt once the asset is stabilized. Munshi Capital Inc. acts as a strategic facilitator in this process, helping you move seamlessly from Fix and Flip Loans into permanent financing like DSCR or conventional mortgages. Having this transition planned from day one ensures you aren't left scrambling when your initial loan term nears its end. If you are ready to accelerate your portfolio growth, you can secure your next deal with Munshi Capital Inc. and experience a streamlined path to funding.

Beyond the Transaction: Partnering with Munshi Capital Inc.

Identifying reliable hard money lenders is a foundational step, but selecting a strategic partner who understands the trajectory of your entire portfolio is what drives long-term wealth. Munshi Capital Inc. operates as more than a source of liquidity; we act as a visionary guide for your real estate ambitions. Led by licensed mortgage professional Amish Munshi (NMLS# 2049293), our firm bridges the gap between the rapid execution of private capital and the long-term stability of institutional financing. We don't just fund isolated transactions. We facilitate results by combining deep market intelligence with the tactical agility required to navigate complex investment environments. Our partnership model ensures that you aren't merely completing a deal; you are building a scalable enterprise supported by executive-level financial expertise.

Our "Main Street Minds" philosophy represents a commitment to transparency and operational efficiency. We recognize that in a high-stakes market, your time is your most valuable asset. By removing the friction often associated with traditional banking, Munshi Capital Inc. allows you to focus on identifying opportunities while we handle the sophisticated mechanics of the debt structure. This proactive approach instills a sense of security, allowing you to move with the gravity required for high-level financial decisions while maintaining a personalized, collaborative edge that suggests a partnership rather than a cold transaction.

Tailored Solutions for Every Investor

The needs of a first-time flipper differ significantly from those of a seasoned fund manager. Our diverse product suite is designed to support you at every stage of the investment lifecycle. Whether you require Bridge Loans for a rapid acquisition or want to stabilize an asset with DSCR Loans, we provide the specific tools needed for your success. Our offerings extend beyond private capital to include Conventional Loans, FHA Loans, and Jumbo Loans. This comprehensive range allows you to transition seamlessly from the high-velocity acquisition phase into permanent, low-cost debt without switching firms. Munshi Capital Inc. understands the nuances of the 2026 national real estate market and customizes every loan structure to align with your specific exit strategy.

Start Your Next Deal with Confidence

Confidence in real estate comes from knowing your funding is secure and your facilitator is proactive. Our streamlined process is designed for speed, ensuring that you can move from a quote to a fast close without the institutional red tape that stalls traditional deals. We prioritize clear communication and actionable outcomes, providing you with the certainty needed to win bidding wars and secure off-market assets. If you're ready to elevate your investment strategy, Consult with Munshi Capital Inc. to secure your private funding today. Establishing a long-term partnership with a facilitator who values your time is the most effective way to turn market opportunities into realized results.

Tactical Execution for Future Growth

The 2026 real estate landscape rewards those who move with precision and speed. Success in this environment requires a shift from a transactional mindset to a strategic one. You've learned that asset-based capital is a tactical advantage for securing distressed properties and winning competitive bids. By prioritizing a robust exit strategy and understanding the total cost of speed, you position yourself as a sophisticated operator. The choice of hard money lenders shouldn't be about desperation; it's about the calculated deployment of capital to capture market opportunities.

Selecting a partner who can facilitate your entire investment lifecycle is essential. Munshi Capital Inc. provides the expert guidance of NMLS-licensed professionals (NMLS# 2049293 and 2250879) to help you navigate complex environments. Our comprehensive product suite allows you to bridge the gap between initial acquisition and long-term stabilization. Whether you require fast-closing Hard Money, flexible DSCR financing, or stable Conventional loans, we possess the market intelligence to drive your results. Stop losing deals to slow institutional approvals and start building with confidence.

Partner with Munshi Capital Inc. for your next real estate acquisition. Your portfolio's next phase of growth starts with the right capital structure and a visionary guide at your side.

Frequently Asked Questions

What is the typical interest rate for hard money lenders in 2026?

Interest rates for hard money lenders in 2026 generally range between 9.5% and 12.5% for experienced borrowers. These rates are a reflection of the speed and flexibility provided by private capital compared to traditional institutional debt. While higher than conventional mortgages, this cost is treated by strategic investors as a tactical expense to secure high-margin opportunities that require immediate funding.

Can I get a hard money loan with bad credit?

Yes, you can secure funding even with a suboptimal credit history because the loan is primarily collateralized by the property itself. Private lenders prioritize the asset's value and your specific exit strategy over historical FICO scores. This asset-based approach provides a vital path for self-employed professionals or investors who are currently rebuilding their financial profiles while pursuing viable real estate projects.

How fast can a hard money lender actually fund a deal?

A professional lender can typically fund a deal within 3 to 5 business days once the initial property evaluation and title work are complete. This rapid execution is the primary reason investors utilize private capital for time-sensitive acquisitions or foreclosure auctions. This timeline is significantly faster than the 30 to 45 days required by traditional banks, providing you with a decisive competitive advantage.

What is the difference between a bridge loan and a hard money loan?

A bridge loan is a functional category of financing used to cover a gap until permanent funding is secured. Hard money is a specific type of bridge loan that is funded by private individuals or companies rather than banks. While the terms are often used interchangeably in real estate, hard money specifically denotes the asset-based nature of the underwriting process and the private source of the capital.

Do hard money lenders require a down payment?

Most lenders require a down payment of 20% to 30% to ensure the borrower has sufficient equity in the project. This requirement protects the interests of both parties and ensures the project is grounded in realistic financial expectations. Some experienced operators may qualify for higher leverage, such as 90% of the purchase price, depending on the property's After-Repair Value and the borrower's track record.

How do I refinance out of a hard money loan once my project is done?

You can transition out of short-term capital by refinancing into long-term debt such as DSCR Loans or Conventional Loans. This process typically occurs once the property is renovated and stabilized with a tenant. Munshi Capital acts as a strategic facilitator in this transition, helping you move from high-velocity acquisition funding into sustainable, low-cost permanent financing to preserve your long-term wealth.

What happens if I cannot pay back a hard money loan on time?

If you cannot meet the repayment deadline, the lender may initiate foreclosure proceedings to recover their investment through the sale of the property. Because the real estate asset serves as the primary collateral, the lender has a direct claim to the property in the event of a default. It's essential to maintain transparent communication with your facilitator to explore loan extensions if your project timeline experiences unexpected delays.

Are hard money loans available for primary residences?

No, hard money loans are almost exclusively designed for investment properties and commercial purposes. Federal regulations for owner-occupied housing are significantly more stringent and are better served by FHA Loans or traditional conventional mortgages. These private capital tools are specifically engineered for the business of real estate investment where speed and property condition are the primary considerations.

© Copyright 2025. Munshi Capital Inc. All rights reserved.