Address: 3100 Oak Rd STE 120 Walnut Creek CA 94597

Call: 877-343-7379

Email: info@munshi.biz

We value your time

Learn the secrets of mortgage world and save on your most expensive budget item!

Eager to know more on how to save on your mortgage?

join us to learn more

Information you were waiting for is available right here! From first time home buyers to seasoned investor and fund managers rely on this information to make informed decisions about their real estate financing.

Mastering the Loan Calculator: A Strategic Guide to Mortgage Planning in 2026

A mortgage calculator is not just a digital convenience; it is a high-precision instrument that determines the viability of your next major investment. Many homeowners and investors treat these tools as simple estimators, only to find their budgets decimated by variables like Private Mortgage Insurance or escalating HOA fees. It's understandable to feel overwhelmed by the technicalities of modern financing, especially when trying to find a reliable loan calculator mortgage estimate that accounts for the current 6.59% average interest rates and the 2026 conforming loan limit of $832,750.

We'll show you how to leverage these tools as strategic assets to forecast exact monthly payments and evaluate total interest obligations over time. You'll gain the clarity needed to distinguish between conventional products and specialized options like DSCR or bridge loans. This guide provides the tactical framework to move from uncertainty to a definitive, budget-aligned financing strategy that secures your financial future in a stabilizing market.

Key Takeaways

- Understand how a loan calculator mortgage tool serves as a risk mitigation asset to ensure financial transparency before you enter the underwriting phase.

- Master the "PITI" components to gain a comprehensive view of your total monthly obligation beyond just principal and interest.

- Learn to adjust inputs for specific loan products like FHA and DSCR to account for unique factors such as mortgage insurance premiums or debt service ratios.

- Identify and avoid the common pitfalls of underestimating closing costs and relying on generic interest rates that don't reflect your unique credit profile.

- Discover how to transition from raw calculations to a refined funding strategy through professional loan origination and expert guidance.

The Strategic Role of a Mortgage Loan Calculator in 2026

A sophisticated loan calculator mortgage tool is a prerequisite for financial transparency in a market defined by elevated but stable interest rates. It functions as a primary mechanism for risk mitigation. By inputting precise variables early in the process, you transform a vague property interest into a concrete financial projection. This proactive approach ensures that your expectations align with the technical realities of modern lending. It's about moving beyond curiosity and toward a definitive commitment.

Precision at the outset is the most effective defense against "deal fatigue" during the underwriting phase. When initial estimates are inaccurate, the subsequent corrections required by lenders can create friction and uncertainty. This often leads to missed deadlines or abandoned opportunities. A Mortgage calculator allows you to stress-test your budget against various scenarios before a single document is signed. It bridges the gap between a simple payment estimate and a comprehensive total cost of capital analysis.

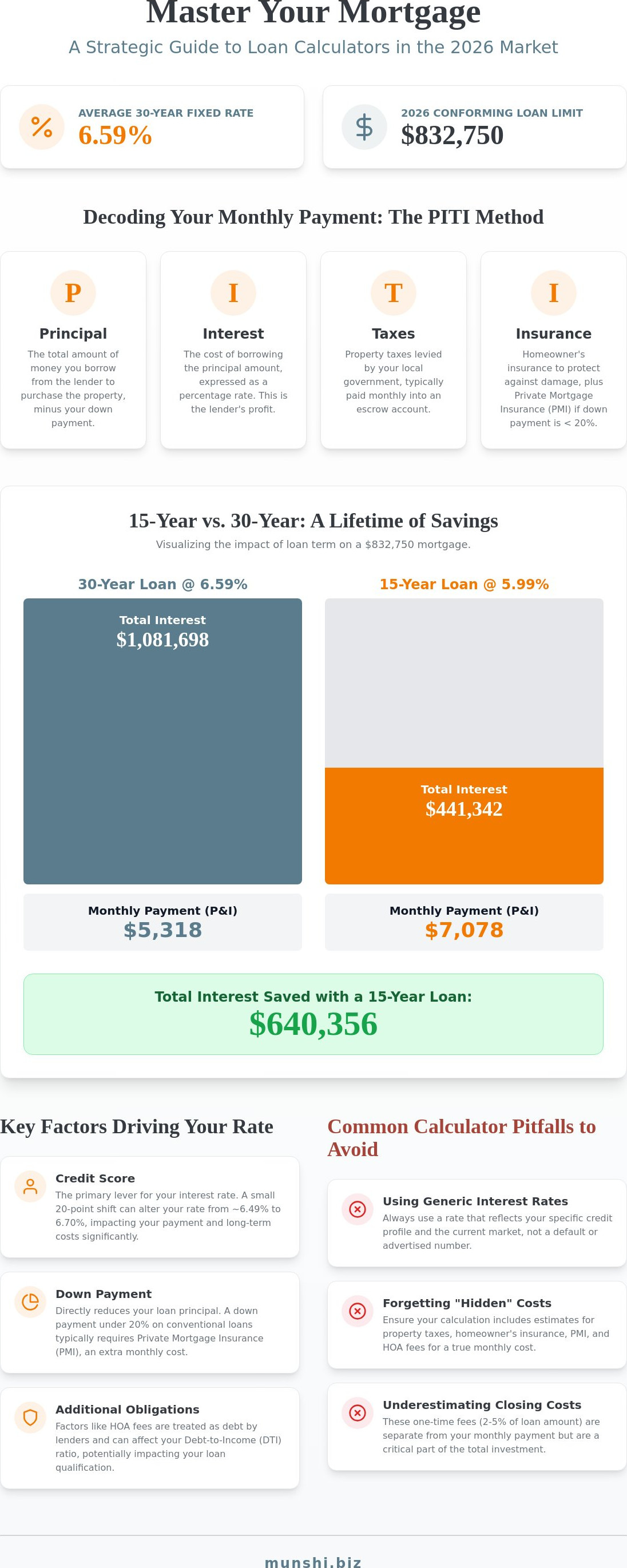

Market dynamics in 2026 demand this level of scrutiny. With the average 30-year fixed rate hovering around 6.59%, the margin for error has narrowed significantly. You aren't just calculating a monthly check; you're evaluating the efficiency of your debt. This strategic foresight is what separates a standard homebuyer from a successful real estate investor. It's the difference between reacting to market shifts and positioning yourself to capitalize on them.

Why Precision Matters in Real Estate Forecasting

Small fluctuations in interest rates are not merely rounding errors. They represent tens of thousands of dollars in lifetime costs. For example, a difference of just 0.25% on a loan at the 2026 conforming limit of $832,750 creates a massive shift in your financial obligation. Accurate calculations facilitate a direct comparison between loan products like FHA and Conventional options, revealing which structure offers the most utility. Amortization is the process of paying off debt through regular installments over time, and understanding its trajectory is vital for long-term planning.

Beyond the Monthly Payment: Analyzing Total Interest

A calculator reveals the hidden impact of your repayment strategy. It allows you to visualize how extra principal payments accelerate equity growth and reduce total interest expenses. When you use a loan calculator mortgage interface, you can see the immediate benefit of shortening your term. Many borrowers find that the trade-off between a 15-year term at approximately 5.99% and a 30-year term at 6.59% is the difference between wealth preservation and unnecessary expenditure. Use these tools to determine your break-even point for future refinancing. This ensures that every dollar spent on interest is a calculated decision rather than a mandatory loss.

Decoding the Variables: What Actually Drives Your Mortgage Payment?

A monthly mortgage payment is a composite figure, not a single line item. To achieve financial precision, you must look beyond the sticker price of a property. Lenders utilize the PITI acronym-Principal, Interest, Taxes, and Insurance-to calculate your total obligation. Each variable carries its own weight. Understanding how these components interact allows you to manipulate the loan calculator mortgage inputs to find your ideal financial fit.

Your credit score serves as the primary lever for the interest rate input. In the 2026 market, where the average 30-year fixed rate is approximately 6.59%, even a modest 20-point shift in your credit profile can move your rate between 6.49% and 6.70%. This fluctuation changes your monthly commitment and your long-term wealth accumulation. If your credit profile doesn't align with traditional requirements, you might consider how specialized loan products can provide a more flexible path forward.

The down payment acts as a secondary modifier. It directly reduces the principal and determines if Private Mortgage Insurance (PMI) is required. On conventional loans, a down payment of less than 20% necessitates PMI, adding a monthly premium that provides no equity benefit. Similarly, Homeowners Association (HOA) fees must be factored into your Debt-to-Income (DTI) ratio. Lenders view these fees as mandatory debts. If an HOA fee is too high, it can disqualify you from a loan even if the P&I payment is affordable.

Principal and Interest (P&I): The Core of the Loan

The principal is the raw amount of capital you borrow after your down payment is applied. This base figure, combined with the interest, forms the bedrock of your payment. The interest rate is the cost of borrowing capital, expressed as an annual percentage. When using a loan calculator mortgage, you must decide between fixed-rate and adjustable-rate inputs. Fixed rates offer stability, while adjustable rates may provide lower initial costs at the risk of future volatility. This choice dictates the rhythm of your amortization schedule for decades.

The 'TI' in PITI: Taxes and Insurance

Property taxes and homeowners insurance are often held in escrow and paid by the lender on your behalf. Taxes are generally estimated based on national averages or specific local assessment rates. Insurance is equally critical. It protects the lender's collateral and is a non-negotiable input for an accurate DTI calculation. In high-risk areas, you must also account for supplemental insurance, such as flood or windstorm coverage. These costs are mandatory. Failing to include them in your early projections leads to a distorted view of your actual purchasing power.

How to Use a Calculator for Different Loan Programs

A generic loan calculator mortgage provides a baseline, but specialized financing programs require a more nuanced analytical approach. Every loan vehicle has its own set of variables that can dramatically shift your debt-to-income ratio or cash flow projections. Understanding these distinctions is the difference between a rough estimate and a viable financial blueprint. Whether you're pursuing a primary residence or a high-leverage investment, your inputs must match the specific logic of the loan product.

Calculating for Investment Properties (DSCR)

Investors utilize calculators differently than primary residents. For a Debt Service Coverage Ratio (DSCR) loan, the primary objective is to determine if the property's gross rental income exceeds the PITI. You aren't just looking for a payment; you're looking for a ratio. If the property generates $3,000 in rent and the PITI is $2,400, your DSCR is 1.25. This figure is the metric lenders use to gauge risk and determine your eligibility. It's a fundamental shift from evaluating personal income to evaluating asset performance.

When inputting data for these deals, remember that investor interest rates are typically higher than those for owner-occupied homes. You must adjust your interest rate input accordingly to ensure your cash flow analysis remains realistic. Sophisticated investors prioritize this immediate liquidity over the total interest paid over 30 years. They view the loan as a tool for leverage rather than a long-term debt burden. Accurate modeling here ensures you don't over-leverage on a deal that looks good on paper but fails in practice.

Conventional and FHA Nuances

Standard calculations often overlook the specific insurance structures of government-backed loans. For an FHA loan, you must account for the Upfront Mortgage Insurance Premium (UFMIP). This is often 1.75% of the loan amount and is typically rolled into the principal. If you don't adjust your principal input to include this fee, your monthly payment estimate will be inaccurate. You can Learn more about FHA loan requirements to see how these specific fees and limits impact your total capital requirement.

Conventional loans operate on a different logic. Once you cross the 20% down payment threshold, the Private Mortgage Insurance (PMI) variable is removed entirely. This creates a significant "step-down" in monthly costs that a basic loan calculator mortgage might not automatically reflect. If you're hovering near that 20% mark, use the calculator to see if the reduction in monthly costs justifies a slightly larger down payment.

Jumbo Loans and Short-Term Financing

For high-value properties exceeding the 2026 conforming limit of $832,750, Jumbo loan math applies. These loans often require larger down payments and stricter reserve requirements, which should be factored into your liquidity planning. Conversely, if you're utilizing Bridge or Hard Money loans for a quick acquisition, your calculator should be set to "interest-only." This reflects the reality of short-term capital where principal reduction isn't the primary goal. Instead, you're focused on the carrying cost of the capital during the renovation or transition period.

The 'Hidden' Costs of Homeownership

Even the most advanced loan calculator mortgage tool is only as reliable as the data you provide. Many borrowers treat the resulting number as a final verdict rather than a baseline. This leads to a dangerous disconnect between digital projections and financial reality. Precision requires you to anticipate costs that exist outside the standard PITI framework. Avoiding these common pitfalls ensures your strategy remains robust through the closing process and beyond.

- Underestimating Closing Costs: These typically range from 2% to 5% of the purchase price. Failing to account for this capital requirement can leave you short at the closing table.

- Relying on National Averages: Using the 2026 average rate of 6.59% is a mistake if your specific credit profile warrants a different tier. Your personal data is the only metric that matters.

- Ignoring Maintenance and Utilities: A mortgage payment is merely the cost of the debt. It doesn't include the ongoing capital needed to preserve the asset's value.

- Disregarding Tax Reassessments: Property taxes often jump significantly after a title transfer. Your calculator must reflect future assessments, not just current ones.

- Overlooking Escrow Volatility: Rising insurance premiums can create escrow shortages. These shortages lead to unexpected spikes in your monthly obligation.

A calculator's monthly payment is not your total cost of living. It is a debt service figure. For real estate investors, this distinction is even more critical. You must account for capital expenditures (CapEx) to ensure your cash flow remains positive during major repairs. Maintaining a buffer in your debt-to-income calculation provides the agility needed to handle market shifts without compromising your stability. If you're ready to move beyond estimates, consult with the expert team at Munshi Capital Inc. to refine your funding strategy.

Interest Rate Volatility and Timing

Market movements don't stop once you find a property. Rate locks are essential to protect your calculated payment during the closing period. It's also vital to distinguish between the Note Rate and the APR. APR includes both the interest rate and lender fees, providing a truer cost of borrowing. This transparency allows for a more accurate comparison of different loan products. Understanding these nuances prevents late-stage surprises and ensures your deal remains financially sound. Using a loan calculator mortgage interface effectively means looking at the total cost of capital, not just the starting rate.

From Calculation to Closing: Leveraging Munshi Capital’s Expertise

A digital loan calculator mortgage tool is an essential first step, but it marks the beginning of your journey, not the end. Raw data provides a foundation. A strategic partner provides the execution. Transitioning from an online estimate to a formal loan origination requires a shift from theoretical math to tactical reality. Munshi Capital Inc. specializes in refining your initial projections into a viable, high-performance funding strategy that aligns with your long-term wealth objectives.

Our role is to serve as a visionary guide through the complexities of both private and conventional capital. While a tool can tell you what a payment might be, it cannot tell you which loan structure will maximize your internal rate of return. We bridge the gap between institutional stability and the agility required by modern investors. This partnership ensures that your financing is not just a transaction, but a catalyst for growth in a competitive 2026 market.

Why a Tool Cannot Replace a Financial Strategist

Calculators are inherently linear. They operate within fixed parameters that often fail to capture the nuances of a sophisticated deal. A standard loan calculator mortgage interface won't identify "Creative Financing" opportunities like bridge loans or fix-and-flip funding when a conventional path hit a roadblock. It doesn't understand the value of your previous investment experience or the liquidity of your broader asset portfolio. Lenders look at the whole picture. We analyze your experience, your assets, and your specific property goals to find the leverage that a simple algorithm would overlook. To see how we apply this expertise to complex scenarios, you should Explore our Private Lending Strategies.

Secure Your Custom Mortgage Quote Today

Moving from an estimate to a closing table requires precision and documentation. The next step in your process is securing a formal pre-approval, which transforms your calculated budget into a credible offer. Munshi Capital Inc. streamlines this progression for fast-moving investors and homebuyers alike. We eliminate the friction of traditional banking, prioritizing efficiency and transparent communication. Don't let your strategy stall at the calculation phase. Reach out to our team to receive a personalized analysis of your scenario and a quote that reflects your unique financial profile. You can Contact Munshi Capital Inc. for a tailored mortgage quote and take the definitive step toward securing your next property with confidence.

Moving Beyond the Numbers to Strategic Execution

You've seen how a loan calculator mortgage tool transforms raw data into a tactical roadmap. By mastering the variables of PITI and adjusting for specific loan programs like DSCR or FHA, you gain a competitive edge in the 2026 market. Precision at this stage is the only way to mitigate risk and ensure your investment remains viable over the long term. Digital tools provide the foundation, but high-level financial success requires moving from theoretical math to a definitive commitment.

Munshi Capital provides the NMLS-licensed expertise needed to refine your projections into a high-performance funding strategy. We specialize in complex DSCR and Hard Money scenarios, offering national reach with the personalized service required for executive-level decision-making. We don't just process transactions; we facilitate growth by aligning your capital needs with market intelligence. Get a Professional Mortgage Analysis from Munshi Capital today to bridge the gap between calculation and closing. Your next great investment is within reach when you combine digital precision with a seasoned strategic partnership.

Frequently Asked Questions

How accurate are online mortgage calculators?

They are mathematically precise but only as reliable as the data you provide. Most tools offer a baseline for principal and interest based on standard algorithms. However, they often fail to account for specific lender fees, shifting insurance premiums, or the 2026 conforming loan limits unless you adjust them manually. Treat these results as a strategic forecast rather than a final financial commitment.

What is the difference between a loan calculator and a mortgage quote?

A calculator provides a theoretical estimate based on user-defined inputs, while a mortgage quote is a formal offer from a lender based on verified data. A loan calculator mortgage interface is designed for preliminary planning and scenario testing. A quote requires a credit review and documentation to confirm your actual interest rate, closing costs, and specific loan terms.

Do mortgage calculators include closing costs?

Most standard calculators do not include closing costs in their default monthly estimate. These expenses typically range from 2% to 5% of the property's purchase price and represent a significant upfront capital requirement. You must manually factor these costs into your liquidity planning to ensure you have sufficient funds available at the closing table without compromising your reserves.

Can I use a mortgage calculator for a DSCR loan?

You can use a calculator to determine the PITI, which is the foundational component of the Debt Service Coverage Ratio. For a DSCR loan, your primary objective is to ensure the property's rental income exceeds this monthly debt obligation. Remember to input higher investor interest rates, which generally sit above the primary residence average of 6.59%, to keep your cash flow projections realistic.

How does my credit score affect the calculator results?

Your credit score is the primary lever that dictates the interest rate you should input into the tool. In the 2026 market, a top-tier score secures rates near the 6.59% national average, while a lower score results in higher monthly costs. Small adjustments to this single input can change your total interest obligation by tens of thousands of dollars over the life of the loan.

What is the most important number in a mortgage calculator?

The total monthly PITI is the most critical figure for managing your immediate cash flow. However, for long-term strategic planning, the total interest paid over the life of the loan is equally vital. This number reveals the true cost of your capital. It allows you to evaluate the efficiency of different debt structures and determine which loan product best serves your wealth-building goals.

Should I include property taxes in my mortgage calculation?

You must include property taxes to achieve an accurate Debt-to-Income (DTI) ratio. Taxes are a mandatory part of your monthly housing expense and are almost always held in escrow by the lender. Excluding them from your loan calculator mortgage analysis will result in an artificially low payment estimate that doesn't reflect the reality of your actual financial obligation.

Can a mortgage calculator help me decide between a 15-year and 30-year term?

It is the most effective tool for comparing these two debt structures. A 15-year term, currently averaging around 5.99%, requires higher monthly payments but generates massive interest savings over time. A 30-year term offers more monthly liquidity but increases the total cost of the home. Use the calculator to balance your current lifestyle needs against your long-term equity objectives.

Contact Info

Address: 3100 Oak Rd STE 120 Walnut Creek CA 94597

NMLS# 2250879

877-343-7379

info@munshi.biz

© Copyright 2025. Munshi Capital Inc. All rights reserved.